What Is AML Customer Screening And Why Is It So Important?

Why does customer screening matter? It quickly picks up on potential risks in AML-KYC screening, smoothing out client onboarding and ongoing checks. Let’s learn more.

Customer screening stands as the first port of call in the global fight against money laundering, and it cannot be overlooked. Let’s find out why.

An effective customer screening process –

1. Kick-starts the AML compliance cycle for financial institutions.

2. Enables banks, insurers, and financial services to assess risks from new and existing clients.

3. Blocks connections to illicit activities right from the start.

4. Serves as a gateway to more thorough investigations when needed.

5. Adheres to global regulations, ensuring financial institutions stay compliant and maintain strict security standards.

[Note: Within this article, the terms customer screening, client screening, KYC screening, and AML-KYC screening are used interchangeably. Each term has been applied where it most aptly fits the context and brings clarity to the information provided.]

How Does the AML Customer Screening Cycle Work?

The customer screening cycle encompasses verifying customer identities, assessing risk profiles based on their financial behavior, and continuously monitoring for consistency and potential illicit activities.

1. Customer Identification and Verification

Initially, the identity verification process –

Collects critical customer data like name, address, birth date, and ID numbers.

Verifies details against independent sources for accuracy.

“Is every detail correct?” This question underpins the vigilance needed in client screening.

2. Risk Assessment

Following identification, the risk management –

Assesses customer risk from financial history, transactions, and associations.

Determines the necessary level of due diligence.

Implements Enhanced Due Diligence (EDD) for high-risk customers for deeper investigation.

3. Ongoing Monitoring

This stage confirms the customer’s behavior remains consistent with their profile. –

Ensures customer activity aligns with their risk profile.

Observes changes in account behavior to signal potential illicit activity.

Represents a persistent, evolving process to counteract emerging threats.

Maintains dynamic, vigilant customer screening.

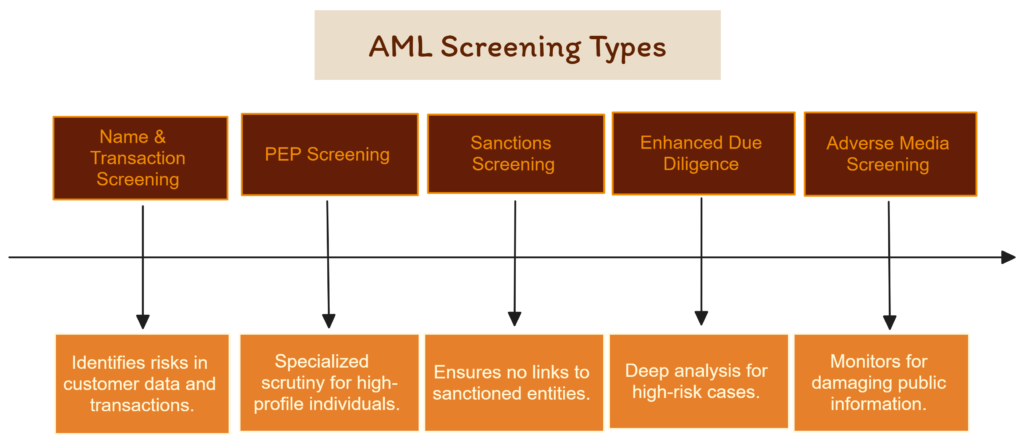

What Are the Different Types of AML Customer Screening?

AML screening isn’t a one-size-fits-all process. Instead, it varies depending on the nature of the risk and the type of customer. Here’s a breakdown of the different types of AML screening that financial institutions commonly use:

1. Name and Transaction Screening

This foundational form of customer screening cross-references customer names and transactions against lists of known criminals, terrorists, or politically exposed persons (PEPs)[point 2 expands on this].

“Could we be inadvertently supporting illegal activities?” This type of KYC screening addresses this vital question, ensuring institutions do not facilitate unlawful operations.

2. PEP Screening

Financial institutions vigilantly monitor individuals who currently hold or have held significant public roles due to the potential risks such roles may carry, including exposure to bribery and corruption.

KYC screening does not stop with the individuals themselves; it also includes their close associates and family members, vital for a complete risk assessment.

Client screening against sanctions is key to maintaining compliance and avoiding hefty penalties.

4. Enhanced Due Diligence (EDD)

High-risk customers—those with substantial transaction volumes, operations in risk-prone countries, or significant political exposure—require deeper investigation.

Monitoring media sources reveals any negative press about potential or current customers.

This method assesses the reputational risk associated with engaging with a particular individual or company.

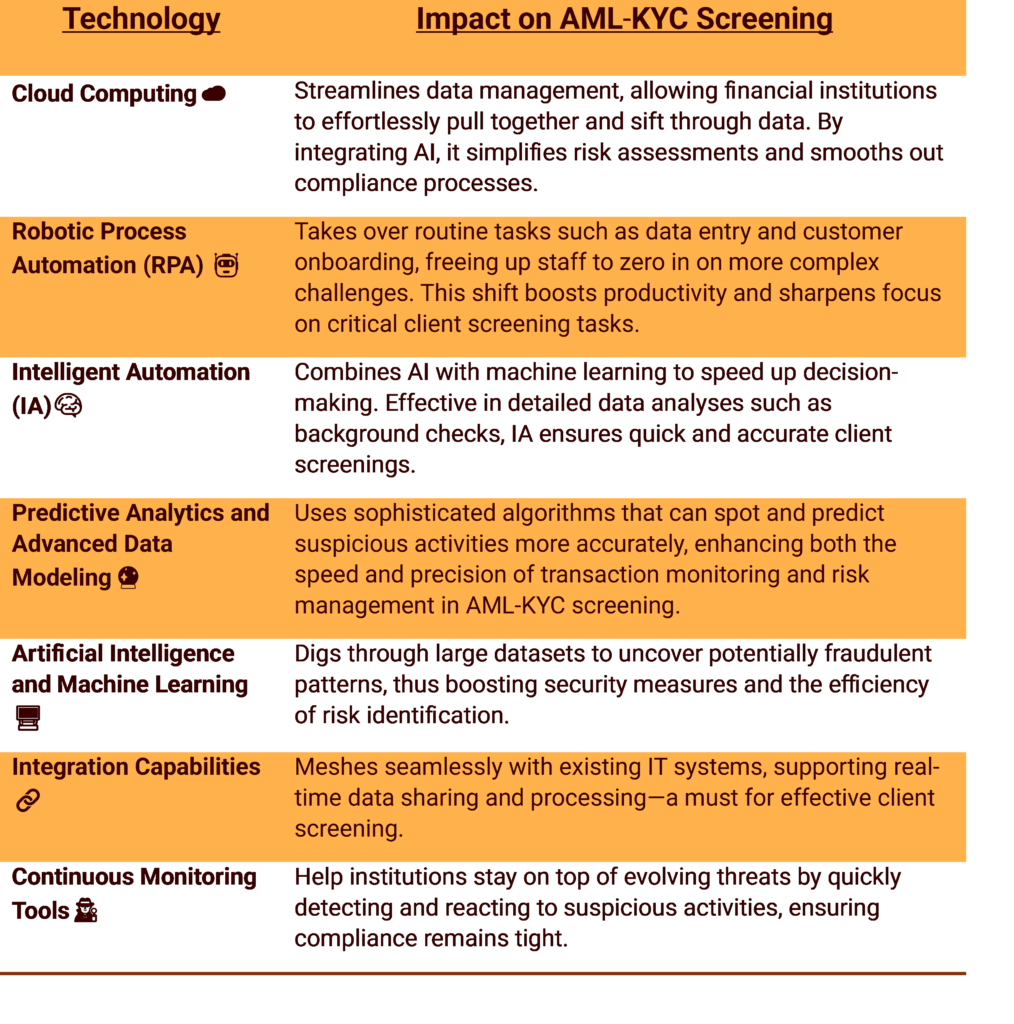

How Do Advanced Technologies Transform AML Customer Screening?

Technology is a game-changer when it comes to effective AML screening. It streamlines processes, enhances accuracy, and helps comply with regulations efficiently.

Here’s how technology is shaping AML screening:

AML-KYC screening tools help financial institutions stay ahead of compliance and risk management, ensuring secure and future-ready systems.

Final Thoughts on Customer Screening in AML

As we peer into the future of Anti-money laundering (AML) efforts, the role of customer screening is poised to become more sophisticated and integral.

What does the future of AML-KYC screening look like with advanced technology and changing regulations?

AI-Driven Accuracy: Machine learning and AI will expedite and refine data parsing, increasing precision and reducing false positives in AML-KYC screening.

Blockchain Transparency: Blockchain will make financial trails clearer, complicating the concealment of illicit funds and bolstering screening.

Regulatory Harmonization: A more unified regulatory landscape will streamline client screening and international financial crime prevention.

Crypto Vigilance: Enhanced tools will target crypto transactions, intensifying scrutiny and risk mitigation.

Compliance Cost Efficiency: Automation, combined with AI, will curtail compliance costs while maintaining rigorous screening standards.

On that note, the evolution of client screening is set against a backdrop of rapid technological advancements and regulatory changes. The journey from traditional methods to more dynamic and integrated approaches is inevitable. As we adapt and innovate, the goal remains clear: to create a financial system that is as secure as it is open to progress.

Stay at the forefront of AML insights and financial crime prevention with ThePerfectMerchant, deeply invested in groundbreaking research. Follow us for the latest updates, or reach out to us — we’re here to help piece together your compliance puzzle.

Top FAQs on AML Customer Screening

What is client screening?

Client screening is the process of verifying the identity of clients and assessing potential risks for money laundering or other illegal activities.

Why is screening important?

Screening is important to ensure financial compliance, prevent identity fraud, and protect against financial crimes like money laundering.

Why is screening done?

Screening is done to fulfill legal obligations, manage risk, and maintain the integrity of the financial system.

When should customer screening be conducted?

Customer screening should be conducted at the start of the client relationship and periodically thereafter, especially when there are significant transactions or changes in customer information.

How often should KYC be done?

KYC should be done initially when a customer relationship is established, and on an ongoing basis to ensure records remain accurate and up-to-date.

How often should KYC be updated?

KYC should be updated at regular intervals, typically every 1-2 years, or when there is a material change in the customer’s circumstances or risk profile.

How KYC prevents money laundering?

KYC prevents money laundering by identifying customers, monitoring transactions, and reporting suspicious activities to authorities, thus disrupting potential laundering schemes.

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…