Customer Due Diligence (CDD) vs. Enhanced Due Diligence (EDD)

Customer due diligence vs. enhanced due diligence—explore the distinctions in this piece. Both are inevitable in managing money laundering risks but vary in depth and scope.

CDD and EDD are important processes to prevent money laundering and terrorism financing. They differ in how detailed the investigations are.

Before getting into details, let’s first cut straight to what is the difference between CDD and EDD with a quick “CDD vs. EDD” comparison chart.

Customer Due Diligence Vs. Enhanced Due Diligence

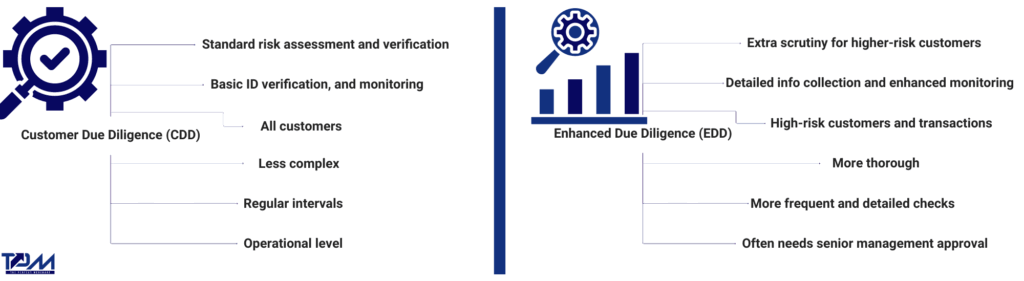

Customer Due Diligence (CDD)

Definition

CDD is the basic process of identifying and verifying a customer’s identity to assess and reduce risks of money laundering and terrorist financing.

Key Components of Customer Due Diligence (CDD)

1. Verify identification: Collect and verify personal details (name, address, date of birth) using reliable sources like government-issued IDs.

2. Identify beneficial ownership: Determine who actually controls a legal entity to understand ownership structures.

3. Conduct risk assessment: Evaluate the customer’s risk level based on their occupation, residential location, and the nature of their relationship with the financial institution.

4. Perform ongoing monitoring: Continuously monitor transactions to identify and report any suspicious behavior promptly.

When Customer Due Diligence (CDD) Is Used

Open new accounts: Conduct CDD when a customer opens a new account to verify their identity and assess their risk level.

Initiate new business relationships: Apply CDD measures when starting a new business relationship to ensure the legitimacy of the entity involved.

Handle large transactions: Perform CDD on large transactions to detect and prevent potential money laundering or terrorist financing activities.

Investigate suspicions of illicit activities: Use CDD when there are suspicions of money laundering or terrorist financing to gather necessary information and report accordingly.

Resolve doubts about previous identifications: Reassess the customer’s information if there are doubts about the accuracy or completeness of previously collected identification details.

Enhanced Due Diligence (EDD)

Definition

EDD involves extra scrutiny and thorough checks for higher-risk customers or transactions, going beyond standard CDD.

Key Components of Enhanced Due Diligence (EDD)

1. Gather detailed information: Collect extensive information about the customer’s background, sources of funds, and purposes of transactions.

2. Implement additional verification: Use multiple sources to verify the collected information, including performing background checks and conducting media searches.

3. Enhance monitoring: Frequently and closely observe transactions and activities to detect any unusual or suspicious patterns.

4. Obtain senior management approval: Require approval from senior management before initiating or continuing relationships with high-risk customers.

When Enhanced Due Diligence (EDD) Is Used

Assess customers from high-risk regions: Implement EDD for customers originating from high-risk countries or regions to mitigate elevated risks associated with these areas.

Evaluate politically exposed persons (PEPs): Apply EDD to PEPs due to their increased risk of involvement in corruption or other financial crimes.

Analyze complex ownership structures: Conduct EDD on entities with complex ownership structures to uncover the true beneficial owners and associated risks.

Scrutinize unusually large or complex transactions: Use EDD for transactions that are unusually large or complex to ensure they are legitimate and not associated with illicit activities.

Enhance measures when CDD is insufficient: Resort to EDD when standard CDD measures are not sufficient to fully assess the risk posed by a customer or transaction.

Due Diligence From the Global Compliance Perspective

Both customer due diligence and enhanced due diligence are essential for following anti-money laundering laws and stopping financial crimes globally. When considering customer due diligence vs. enhanced due diligence, it’s clear that both are indispensable.

The “CDD vs. EDD” comparison isn’t about choosing one over the other. Instead, it highlights how each plays a unique role in helping businesses adhere to local and international regulations, keeping the financial system secure.

Financial Action Task Force (FATF) on CDD and EDD

The Financial Action Task Force (FATF) sets international standards for combating money laundering and terrorist financing.

According to FATF’s recommendations:

Customer due diligence is mandatory in AML processes (Recommendation 10).

Enhanced due diligence is specifically required for higher-risk scenarios, such as business relationships and transactions involving individuals or entities from high-risk countries (Recommendation 19).

The latest FATF reports emphasize the importance of CDD and EDD in anti-money laundering (AML) compliance:

1. Increased monitoring for strategic AML deficiencies: Jurisdictions like Monaco and Venezuela are under increased monitoring for strategic AML deficiencies, requiring enhanced due diligence measures.

2. Revised criteria for FATF reviews: Updated criteria for FATF reviews now include stronger CDD and EDD requirements to ensure countries can trace and recover criminal assets effectively.

3. High-risk jurisdictions with serious AML deficiencies: Countries with serious AML deficiencies are subject to enhanced due diligence and, in severe cases, counter-measures to protect the international financial system.

Regulatory penalties for non-compliance: Non-compliance with CDD and EDD requirements can result in significant penalties, including hefty fines and the suspension of business licenses. Regulatory authorities emphasize the importance of robust due diligence processes to avoid legal and financial repercussions.

CDD and EDD From the Technological Perspective

Automated media screening and global databases for sanctions, peps and adverse media help identify hidden risks and maintain compliance.

Technology integration: Uses automation, AI, and data analytics to perform thorough checks and meet regulatory requirements.

Automated EDD: Manages large data volumes efficiently, reducing errors and focusing on high-risk profiles.

Adverse media and negative screening: Searches for negative news, sanctions lists, and regulatory actions to quickly identify risks.

Ongoing monitoring and record-keeping: Continuously monitors transactions and updates records to ensure compliance.

Final Thoughts on CDD vs. EDD

CDD vs. EDD: Essential for effective AML/CTF compliance. CDD provides basic checks, while EDD involves more detailed checks for high-risk customers.

Different industries may require specific EDD measures, particularly in high-risk areas such as dealing with PEPs or cash-intensive operations.

For more information, such as customer due diligence vs. enhanced due diligence, we encourage you to visit ThePerfectMerchant. We would love to hear from our readers and help troubleshoot compliance together. Contact us here.

Top FAQs on CDD vs. EDD

What is CDD, SDD, and EDD?

CDD (customer due diligence) checks who the customer is and their risk level. SDD (simplified due diligence) is a lighter check for low-risk customers. EDD (enhanced due diligence) is a detailed check for high-risk customers with more documentation and monitoring.

What is the KYC, CDD, and EDD process?

KYC (Know Your Customer) is the process of verifying who the customer is. CDD is the standard check within KYC. EDD is a more detailed check for high-risk customers.

What are the 3 types of customer due diligence?

The three types are simplified due diligence (SDD) for low-risk customers, customer due diligence (CDD) for most customers, and enhanced due diligence (EDD) for high-risk customers.

What is the difference between CDD and EDD (in a nutshell)?

CDD is a basic check to verify a customer’s identity and assess their risk. EDD is a thorough check for high-risk customers, with extra steps and continuous monitoring.

What is the difference between simplified due diligence and enhanced due diligence?

Simplified due diligence (SDD) involves basic checks for low-risk customers. Enhanced due diligence (EDD) involves detailed checks and more documentation for high-risk customers.

What are the two types of CDD?

The two types are standard due diligence, for regular customers, and simplified due diligence, for low-risk customers.

What is EDD in banking terms?

EDD (enhanced due diligence) in banking means extra detailed checks for high-risk customers to comply with anti-money laundering (AML) rules.

What is CIP vs. CDD vs. EDD?

CIP (Customer Identification Program) is about verifying customer identity. CDD checks identity and assesses risk. EDD is a detailed check for high-risk customers.

What is the difference between ECDD and KYC?

ECDD (enhanced customer due diligence) is another term for EDD, meaning detailed checks for high-risk customers within the KYC (Know Your Customer) process.

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…