Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk.

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk.

What Is a Red Flag in AML?

A red flag in anti-money laundering (AML) is a warning sign that something suspicious might be happening. It could mean someone is trying to hide illegal money through transactions or shady business activities.

When financial institutions spot AML red flags, they need to look closer and figure out if there’s anything unlawful going on.

What Are the Common Indicators for AML Red Flags

Red flags can pop up in many ways. They’re like clues that point to risky or unusual behavior. Here are some common signs:

Strange transactions: Many small transactions that stay just below reporting limits.

Hidden owners: People or businesses hiding who really owns an account.

Lots of cash: Big deposits or withdrawals in industries that don’t normally use a lot of cash.

Unexplained wealth: Sudden spikes in wealth with no clear source.

Is There Any Global List of AML Red Flags

While AML red flags are not globally uniform, the Financial Action Task Force (FATF) provides broad guidance. Some internationally recognized red flags include:

High-risk countries: Transactions involving places with weak AML laws.

Structured payments: Breaking big sums into smaller pieces to avoid getting noticed.

Mismatched information: What a customer says doesn’t line up with what they do.

What Are Red Flags In AML-KYC?

KYC, or Know Your Customer, helps businesses understand who they’re working with. During this process, red flags include:

Reluctance to share information: Customers avoid answering questions or giving documents.

Complicated ownership: Businesses with confusing structures to hide who’s really in charge.

Politically exposed persons (PEPs): People in powerful positions who might be at higher risk for corruption.

What Are the Money Laundering Red Flags for Banks

Banks are usually the first to catch suspicious behavior. Here’s what banks need to watch for:

High-risk accounts: Clients from industries with a history of financial crimes, like casinos.

Multiple accounts: A customer opens many accounts for no clear reason.

Frequent international transfers: Big transfers to other countries without a clear business reason.

Correspondent Banking AML Red Flags

Correspondent banking—when one bank provides services to another—can come with risks. Watch out for these warning signs:

Shell banks: Payments from banks that only exist on paper, with no real offices.

Layered transactions: Payments moving through multiple banks to hide their origin.

Sanctioned entities: Transactions involving people or companies on global sanctions lists.

BSA AML Red Flags

The U.S. Bank Secrecy Act (BSA) helps stop money laundering by requiring banks to report suspicious activity. Here are key red flags:

Smurfing: Customers making lots of small deposits to stay under reporting limits.

Wire transfers: Frequent transfers to high-risk countries.

Third-party transactions: Using someone else’s account to hide where money is coming from.

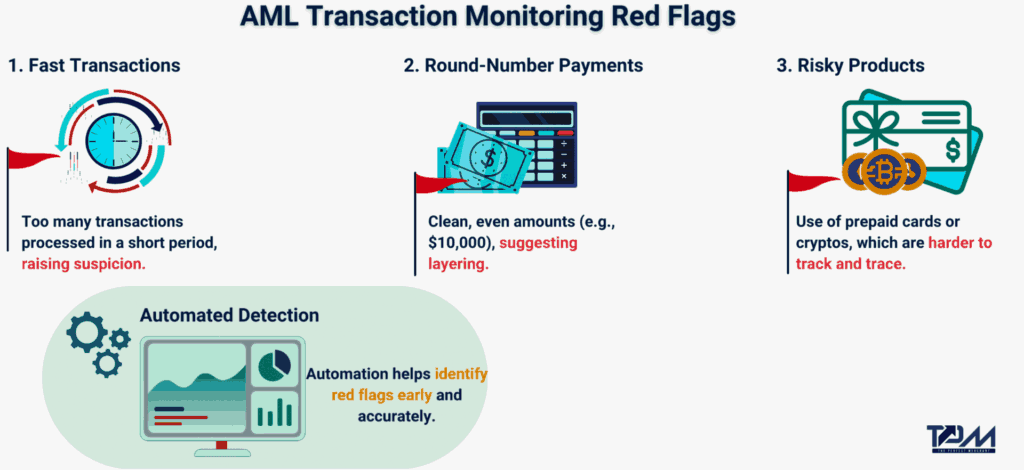

What Are the Major AML Transaction Monitoring Red Flags

Many businesses use automated systems to track transactions. These systems flag activities that don’t feel right, such as:

Fast transactions: Lots of transactions in a short time.

Round-number payments: Transfers with neat, round amounts, which might suggest layering.

Risky products: Use of prepaid cards or cryptocurrencies, which are harder to trace.

Code Snippet: Automating AML Red Flag Detection in Python

To keep up with evolving risks, many financial institutions rely on automated transaction monitoring systems. Below is a sample Python code snippet that demonstrates how a bank might use simple logic to flag suspicious transactions based on common red flags.

# Example: Simple AML Transaction Monitoring Logic

# List of suspicious countries

high_risk_countries = ["North Korea", "Iran", "Syria"]

# Function to check for suspicious transactions

def is_suspicious(transaction):

# Unusual transaction size

if transaction["amount"] > 10000:

return True, "Transaction amount exceeds threshold"

# Check if the transaction involves a high-risk country

if transaction["country"] in high_risk_countries:

return True, "Transaction involves a high-risk country"

# Round-number transaction

if transaction["amount"] % 1000 == 0:

return True, "Round-number transaction detected"

return False, "Transaction is normal"

# Sample transaction data

transactions = [

{"id": 1, "amount": 5000, "country": "USA"},

{"id": 2, "amount": 15000, "country": "North Korea"},

{"id": 3, "amount": 3000, "country": "Germany"},

{"id": 4, "amount": 20000, "country": "Syria"}

]

# Process transactions and flag suspicious ones

for txn in transactions:

suspicious, reason = is_suspicious(txn)

if suspicious:

print(f"Transaction {txn['id']} flagged: {reason}")

else:

print(f"Transaction {txn['id']} is normal.")

Explanation of code snippet

The code above checks for three common AML red flags:

1. High transaction amount: Transactions above a defined threshold (e.g., $10,000).

2. High-risk countries: Involvement of countries with weak AML controls.

3. Round-number transactions: Payments made in neat, rounded amounts, which may indicate layering.

This snippet shows a simple way to analyze transactions, but real-world systems use machine learning models and advanced analytics for more accuracy. Banks often combine these automated checks with manual reviews to ensure they catch suspicious activities.

Final Note on AML Red Flags

AML red flags are both generic and customized in nature. Depending on your nature of business, geographic location, and regulations, the AML red flags indicator list must be kept updated.

To adopt a tailormade approach on AML red flags, you may contact ThePerfectMerchant as we help businesses draft custom-made risk indicators specific to their businesses.

AML risk indicators show where there might be a chance of money laundering. These include large cash transactions, unusual account activity, hidden ownership, or dealing with high-risk countries.

What are the 5 red flags of AML?

The top red flags are unusual transactions, high-risk countries, sudden wealth with no reason, frequent small deposits, and round-number payments. They hint at attempts to avoid detection.

What are the red flags for AML gambling?

In gambling, red flags include players making large cash deposits, using multiple accounts, cashing out quickly without much play, or gambling just enough to turn illicit money into legitimate funds.

What are the red flags for funds transfer?

Look out for repeated small transfers, cross-border payments without clear purpose, large transfers with no business reason, or transactions involving high-risk countries.

When should an AML concern be escalated?

You escalate an AML concern when transactions look suspicious, customers avoid giving information, or patterns hint at illegal activity. Quick action helps prevent money laundering.

What are the red flags for insurance money laundering?

These include overpaying premiums, purchasing policies with cash, quickly canceling policies for refunds, or naming beneficiaries who aren’t clearly related to the policyholder.

What are the red flags for AML brokerage?

Watch for clients making frequent trades with no strategy, transferring funds between accounts often, or handling large sums through offshore accounts without a clear reason.

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…