AML Data: The Foundation of Modern Financial Crime Prevention

Learn why anti-money laundering data, or AML data, is considered an asset to all AML-obligated businesses. Explore data dependency with case studies and data best practices to overcome AML challenges.

So, what exactly is AML data? It’s the information companies gather to detect illegal money movements, prevent them from spreading, and stay in line with anti-money laundering (AML) regulations.

Anti-money laundering data plays a key role in compliance programs. If someone tries to move dirty money through the system, this data is what helps organizations identify and block it. Since financial criminals are always searching for weak spots, having reliable AML data keeps businesses prepared.

By using anti-money laundering data effectively, companies can separate normal financial activity from risky behavior. This reduces the chance of facing unexpected fraud that could damage their reputation or lead to serious consequences.

In this article, we’ll lay hands on:

Internal AML data (KYC, transaction, SARs and risk data).

External AML data (public, sanctions, PEP, adverse media data).

Internal and external AML data codependency.

AML data case studies (with SQL and Python code snippets).

AML data best practices to overcome implementation challenges.

Now, let’s begin!

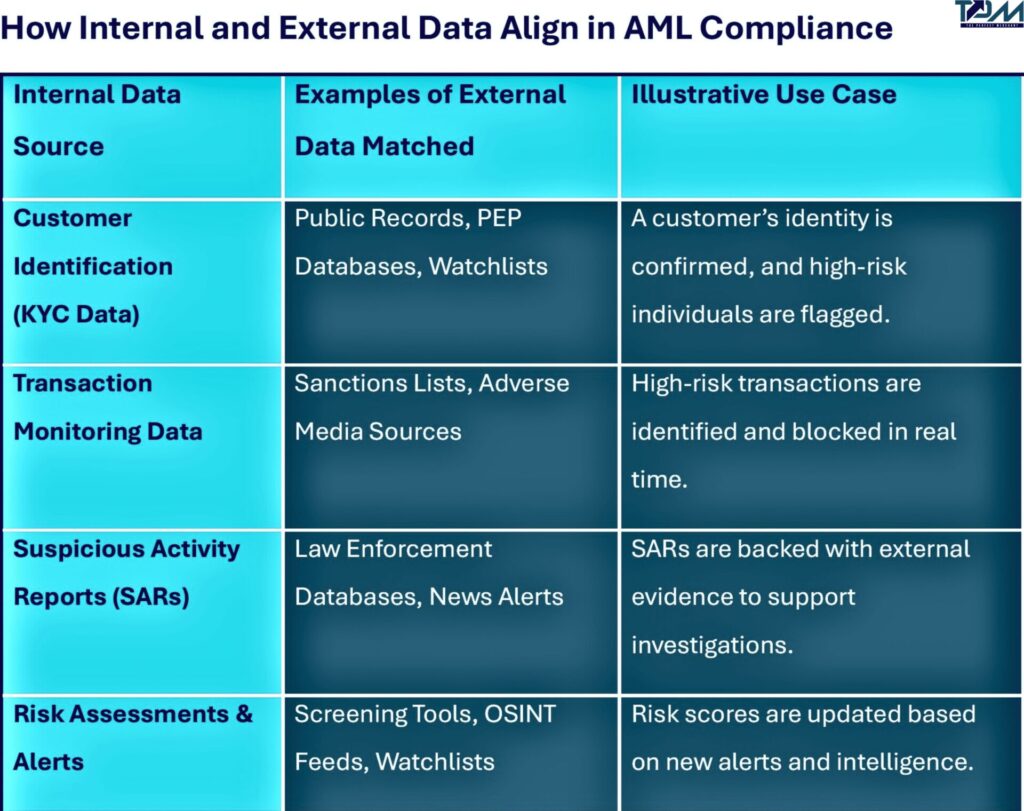

Internal AML Data Sources [To Watch For]

This is the information you collect and manage inside your organization—tracking what customers do from the moment they join to how they behave over time. While this data is under your control, it gains value when validated against external sources (covered in the next section).

In the context of internal anti-money laundering data, here’s what you need to keep an eye on:

Customer Identification Data (KYC)

All the basics you collect during onboarding—like names, addresses, birthdates, and nationalities. This is how you know exactly who you’re dealing with and confirm they are who they say they are.

Transaction Monitoring Data

Records of every financial move your customers make—deposits, payments, wire transfers, withdrawals. This data helps spot patterns or activities that look out of place.

Suspicious Activity Reports (SARs)

Internal red flags raised when something doesn’t add up. If your team finds a transaction sketchy, SARs make certain it’s reported to regulators on time.

Risk Assessments & Alerts

Warnings generated when something raises a compliance eyebrow. It might be a high-risk customer or unusual transaction patterns—your internal models bring these risks to light.

External AML Data Sources [To Tap Into]

External data complements your internal AML data—it validates, enhances, and fills in gaps. Thus, it makes your AML efforts stronger and more complete.

Here’s what you rely on:

Law Enforcement and Public Databases

Police reports, court records, and government-verified identity information help identify risky customers.

Example: A financial institution checks public records to confirm a customer’s identity and uncover any criminal history.

Case Example: A bank reviews a new account and flags it due to the applicant’s presence on a PEP list, triggering due diligence.

Adverse Media Alerts

Real-time alerts from news sources and open-source intelligence (OSINT) flag negative news or criminal connections.

Illustration: A compliance team follows up on a media alert linking a client to illegal activities. This red flag leads to a manual review of the client’s recent transactions.

Why the Split—and the Connection—Matters

While internal and external data sources have distinct roles, they work in synergy to meet AML obligations. Internal data tells you what’s happening within your organization, while external data validates, enriches, and enhances that story with critical outside information.

This interplay ensures your compliance program is both efficient and comprehensive. The data interaction seamlessly blends internal monitoring with external verification.

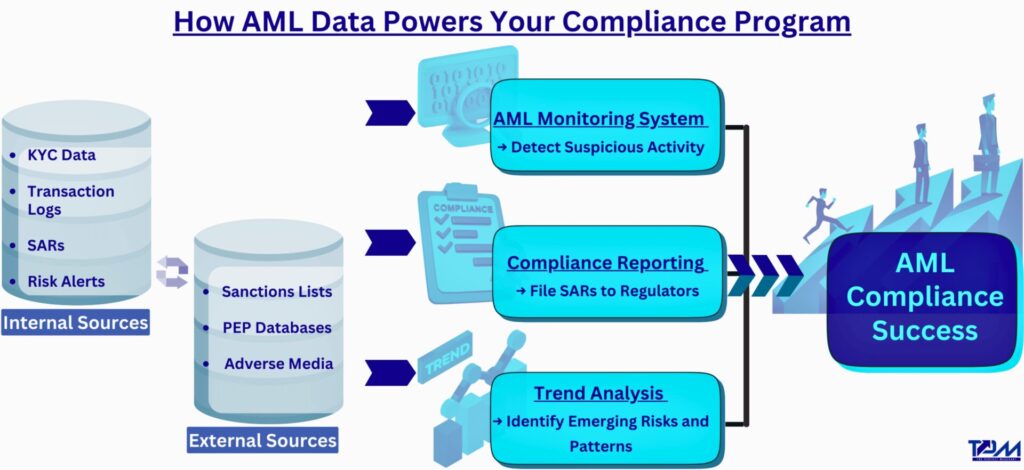

How AML Data Powers Your Compliance Program

Here’s how AML data drives compliance efforts:

Monitoring Transactions

Let’s say a customer starts wiring money to five different countries in a day. That’s a red flag. AML data helps you identify these patterns before things get out of hand.

Compliance Reporting

When regulators ask for suspicious activity reports (SARs), AML data makes sure you have everything in order. Well-prepared reports keep your business in line with the rules and out of trouble.

Trend Analysis

AML data isn’t just about reviewing past transactions—it helps you stay ready for future risks. Recognizing patterns early allows you to handle new money-laundering methods before they become serious issues.

The below image is the summation of everything we have learned about AML data to achieve AML compliance success till now in this article.

AML Data in Action: Case Study Snapshots

To help you see how AML data works in the real world, let’s take a closer look at two practical examples. Consider these as case studies—bite-sized, actionable scenarios showing how you can leverage AML data to make your job easier and stay compliant.

SQL Query to Flag Suspicious Transactions

SQL helps you efficiently monitor big datasets. Here’s a quick query that flags high-value transactions linked to risky countries:

-- Identify transactions over $15,000 in high-risk countries

SELECT

customer_id, transaction_id, amount, transaction_date, country

FROM

transactions

WHERE

amount > 15000

AND country IN ('Iran', 'North Korea', 'Syria')

AND transaction_date >= (CURRENT_DATE - INTERVAL '30' DAY);

This query helps your team spot transactions over $15,000 in high-risk regions—so you know where to focus first.

Once flagged, these transactions can be reviewed and assessed alongside any additional relevant information.

Automating SAR Report Generation with Python

After you’ve flagged suspicious transactions, the next step is reporting. Automating the process saves time and reduces human error. Here’s a Python snippet to generate a SAR report:

import pandas as pd

# Example data for flagged transactions

data = {

"transaction_id": ["TX123", "TX456"],

"customer_id": ["C001", "C002"],

"amount": [20000, 30000],

"country": ["Iran", "North Korea"],

"risk_level": ["High", "High"]

}

# Create a DataFrame from the provided data

df = pd.DataFrame(data)

# Save the SAR report as a CSV file

report_name = "suspicious_activity_report.csv"

df.to_csv(report_name, index=False)

print(f"SAR report generated: {report_name}")

This code ensures flagged transactions are neatly documented in a CSV, ready for submission to regulators.

With this automation, your compliance team can stay organized without getting buried in manual tasks, resulting in timely submissions.

Challenges and Best Practices for Managing AML Data

Okay, so AML data is powerful, but managing it isn’t always a cakewalk. Here are a few bumps you’ll want to watch out for:

✔️Data Overload

There’s a lot of data flying around, and not all of it is useful. In other words, there’s too much data to sift through manually.

Use automated systems to focus on the most relevant activities and flag high-risk behavior in real-time.

✔️Siloed Information

When your data sits in separate systems that don’t talk to each other, you can’t get the full picture.

Keep your data centralized to connect the dots quickly and avoid blind spots.

Schedule regular audits to ensure your data stays clean, accurate, and useful for compliance efforts.

✔️Limited Resources

Compliance teams are often stretched thin.

Invest in the right tools and use automation to improve efficiency. Let your team focus on higher-priority tasks without burning out.

Why AML Data Matters More Than Ever

Financial criminals aren’t slowing down, and neither can you. Good quality AML data—organized, up-to-date, and actionable—is your opportunity to be smarter, faster, and better than the bad guys. From catching fraud early to avoiding regulatory fines, it protects your organization’s reputation. The right data makes all the difference.

If you want more insights into other anti-money laundering data and data sources, follow ThePerfectMerchant. For discussions on AML data intelligence, feel free to contact us—we’d love to hear from you!

Looking for more about specific datasets or the infrastructure behind AML data? Explore our articles on AML datasets and AML databases to investigate more closely how data collections and storage systems work together.

Top FAQs on Anti-Money Laundering Data

What is AML in data?

AML in data refers to the information collected and monitored to stop illegal money movements, like money laundering. This data includes details about customers (KYC), records of transactions, risk evaluations, and reports of suspicious activities.

What are AML records?

AML records store key information like customer identities, their transactions, and any reports filed about suspicious activities (SARs). Banks and companies must keep these records for audits, legal reviews, and investigations by regulators.

What does AML check stand for?

An AML check ensures that people, businesses, and transactions follow anti-money laundering rules. It involves screening names against government sanctions lists, politically exposed persons (PEP) databases, and other warning indicators to catch risks.

What is an AML checklist?

An AML checklist outlines key steps for staying compliant with anti-money laundering rules. This includes customer onboarding, keeping an eye on transactions, and submitting suspicious activity reports (SARs). It helps companies meet legal standards and reduce risks.

What is the red flag in AML?

A red flag in AML signals unusual or suspicious behavior. Examples include large cash deposits, complicated money transfers, or sudden activity in previously inactive accounts. These warning signs prompt compliance teams to investigate further.

What is the AML update for 2024-2025?

The 2024-2025 AML update highlights stricter regulations, tougher KYC rules, and longer sanctions lists. AML-obligated entities need to adapt by using advanced tools to monitor real-time transactions and report SARs.

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…