How To Calculate False Positives in Transaction Monitoring (And Reduce Them)

How to calculate the false positive rate in transaction monitoring? Although completely eliminating them is unlikely, there are methods to reduce false positives in transaction monitoring. Read this article.

Let’s start with a scenario we’ve all seen: a perfectly legitimate transaction gets flagged as suspicious. That’s a false positive, and it’s a headache, especially in our world where AML compliance is non-negotiable.

What are False Positives in Transaction Monitoring?

False positives in transaction monitoring arise when legitimate transactions are wrongly flagged as suspicious or fraudulent by monitoring systems. This is a significant issue in sectors like banking and finance, where compliance with anti-money laundering (AML) regulations is an obligation.

Why False Positives Must Be Addressed Right Away?

We all know that high false positives rate in transaction monitoring can be more than just a nuisance—they can:

✔️ drive up costs,

✔️ strain customer relationships, and

✔️ muddy the waters when trying to detect real fraud.

The faster we address them, the smoother our operations. It requires continuous fine-tuning of the system along with recurrent human interventions. This article gets into a more intense conversation on:

How to calculate false positives in transaction monitoring.

False positives rate in transaction monitoring.

The actual cost of false positives.

How false negatives factor in.

Can we completely eliminate false positives in transaction monitoring?

So, without further ado, let’s get started!

How To Calculate False Positives in Transaction Monitoring

First things first, it’s important to accurately calculate the false positive rate in transaction monitoring.

Correct mathematics helps the risk desk understand the actual impact of false positives on the business. This, in turn, aids in comprehending the necessity of fine-tuning transaction monitoring systems.

False Positives Rate in Transaction Monitoring

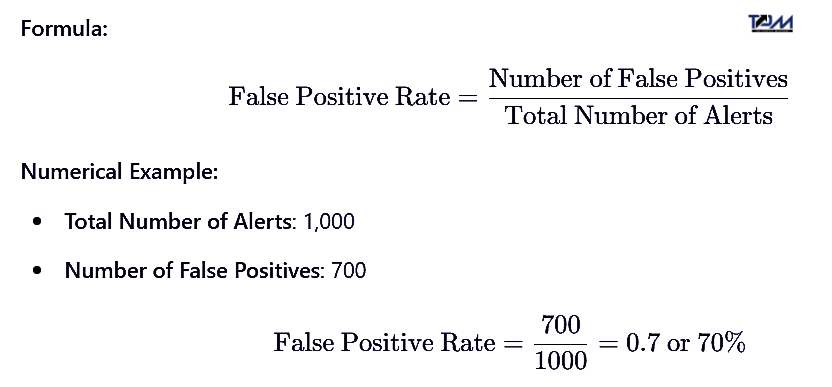

False Positive Rate (FPR): This is straightforward—divide the number of false positives by the total number of alerts. It gives you a clear picture of the proportion of alerts that were flagged as suspicious but turned out to be legitimate.

Interpretation of the above calculation: It means that 70% of the alerts generated by the system were false positives, indicating a high rate of inefficiency where most of the flagged transactions were actually legitimate.

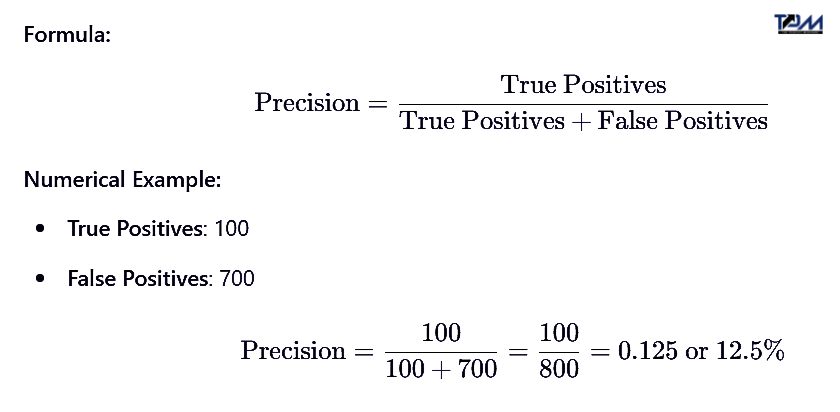

Precision Rate (Alerts Accuracy): Also known as the Positive Predictive Value, it measures how many of the alerts flagged as suspicious were actually true positives (i.e., they were indeed suspicious upon further investigation).

Interpretation of the above calculation: It means that only 12.5% of the alerts that were flagged as suspicious were actually true positives. In other words, the system accurately identified suspicious transactions 12.5% of the time, suggesting there is significant room for improvement in the system’s accuracy.

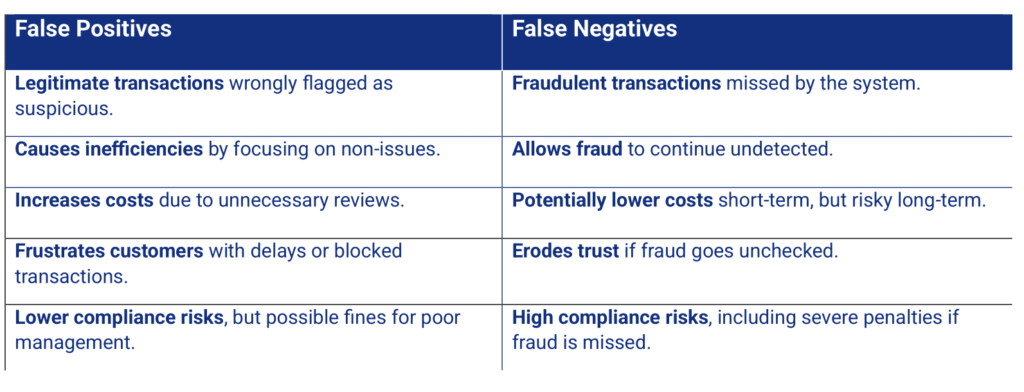

Unlike false positives, false negatives happen when fraud slips through unnoticed. Check out this chart to see how they compare.

Can False Positives in Transaction Monitoring Be Completely Eliminated?

We all know that completely eliminating false positives is a tall order. But significant reductions are achievable.

Challenges to consider:

Evolving fraud tactics: Fraudsters constantly change their methods, making detection challenging.

Tech limitations: Even the best technology can’t catch everything, but improvements are ongoing.

Leveraging Advanced Analytics to Reduce False Positives

To effectively manage false positives, implementing data-driven and adaptive strategies is essential.

1. Use diverse and real-time data sources: Incorporate data from multiple, up-to-date sources, including transaction records and customer profiles to enhance monitoring accuracy.

2. Maintain system accuracy with regular updates: Regularly update your monitoring systems and integrate the latest threat intelligence to ensure accurate detection of suspicious activities.

3.Leverage ML for complex and changing patterns: ML, as part of AI, identifies evolving patterns, reducing false positives where behavior isn’t easily defined.

4. Apply rule-based systems for clear patterns: AI-enhanced rule-based systems effectively handle consistent, predictable scenarios, adjusting to new threats as needed.

5. Implement risk-based approaches: Prioritize alerts based on risk to manage workload efficiently. Advanced screening tools and politically exposed persons (PEP) scoring models can help focus on high-risk cases.

Instead of striving for perfection, aim for consistent, meaningful improvements.

How advanced analytics works:

🔘Predictive modeling: Uses data to identify potential fraud before it occurs, enhancing proactive detection.

🔘Anomaly detection: Spots unusual patterns that deviate from normal behavior, indicating possible fraud.

🔘Continuous learning: Adapts to emerging fraud tactics, ensuring the system remains effective and up to date.

By staying on top of these strategies and tools, you can significantly reduce false positives, ensuring smoother compliance, better customer experiences, and a more efficient fraud detection process.

What’s the Real Costs of AML False Positives?

False positives in AML processes carry both direct and indirect costs —they have real-world costs that hit your bottom line.

Operational Costs: The more false positives, the more resources you’re throwing at manual reviews. It’s a drain on time and money.

Regulatory Risks: Miss managing false positives, and you could face fines from regulators. It’s not a risk worth taking.

Constantly dealing with false positives means your team is stretched thin, leaving less time and energy for identifying actual fraud. It’s a lose-lose situation.

We hope you liked this article on “how to calculate false positives in transaction monitoring”. For more insights on AML, transaction screening, and fraud prevention, follow ThePerfectMerchant on LinkedIn. We value your feedback—feel free to reach out with any questions!

Top FAQs on False Positives in Transaction Monitoring

1. What are false positives in sanction screening?

False positives in sanction screening occur when a system incorrectly flags a legitimate individual or transaction as a match to a sanctions list. This happens due to similarities in names, aliases, or other identifying features between legitimate entities and those on the list.

2. How do false positives impact fraud detection?

False positives can hinder fraud detection by overwhelming compliance teams with a high volume of alerts that are not genuinely suspicious. This diverts attention and resources from investigating actual fraudulent activities, potentially leading to real threats being missed and causing operational inefficiencies.

3. What is an example of a false positives in transaction monitoring?

One of the examples of false positives in transaction monitoring could be a large, one-time transfer made by a legitimate customer, which resembles patterns associated with money laundering. Despite being a legitimate transaction, such as a down payment on a house, the system may flag it as suspicious due to its size or unusual nature.

4. How do you calculate the expected number of false positives?

To calculate the expected number of false positives, multiply the total number of non-suspicious transactions by the false positive rate. For example:

Expected Number of False Positives = Total Non-Suspicious Transactions * False Positive Rate

5. What is a true negative in transaction monitoring?

A true negative in transaction monitoring occurs when a legitimate transaction is correctly identified by the system as not suspicious. This means the system accurately recognizes the transaction as safe and does not flag it for further review.

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…