A Talk on Key Global Anti-Money Laundering (AML) Regulations

Global Anti Money Laundering Regulations: What they are, who regulates them. How are the AML rules drafted to achieve coherent anti money laundering standards?

In international finance, AML compliance regulations are a cohesive response to the insidious threat of money laundering, a threat that knows no borders and spares no economy. The article pivots around the stringent anti money laundering standards that regulated entities worldwide must implement and uphold.

At the core of international anti money laundering regulations is a concerted effort to promote integrity, combat illicit financial flows, and support economic stability. These consensually drafted rules prevent the mingling of ill-gotten gains with legitimate assets and protect the financial infrastructure from being a conduit for financing nefarious activities that undermine national and global security.

So, let’s begin with who regulates global anti money laundering regulations, and try to unfold the complex fabric of AML compliance—a commitment that is as much about legal adherence as it is about promoting the faith of individuals and businesses in the international economy.

Who Regulates Anti-Money Laundering Globally?

The Financial Action Task Force (FATF), a bedrock institution, orchestrates a symphony of AML regulations with a global reach. Its Recommendations resonate through the legal frameworks of over 200 jurisdictions, including the European Union, which rigorously updates its AML directives, and the United States, where the Bank Secrecy Act (BSA), under the vigilant eye of FinCEN, anchors national efforts. Regional entities amplify these standards, ensuring compliance and financial integrity across continents. This global mosaic of AML oversight champions a fortified bulwark against the financial specters of money laundering and terrorism financing.

Furthermore, to fight against economic crimes, the Egmont Group ensures swift information exchange among Financial Intelligence Units. These efforts are complemented by technological strides in tracking illicit transactions, exemplified by the EU’s fifth anti-money laundering directive which tightens the reins on cryptocurrency activities. The synergy between international policy and regional adaptation is key to this robust defense against the financial underworld’s threats.

In the next section, let’s learn about the major AML rules and regulations formed by international bodies and followed by major countries across the world.

Major AML Rules And Regulations Around the World

Adhering to AML regulatory requirements is not just about compliance; it’s a strategic obligation for businesses and financial institutions worldwide. The Financial Action Task Force (FATF) leads the charge in setting international anti money laundering regulations, creating a unified front against financial crimes. This introduction explores the pivotal role of various regulatory frameworks, including AML banking regulations and AML compliance regulations, in defending the financial sector against money laundering and terrorism financing.

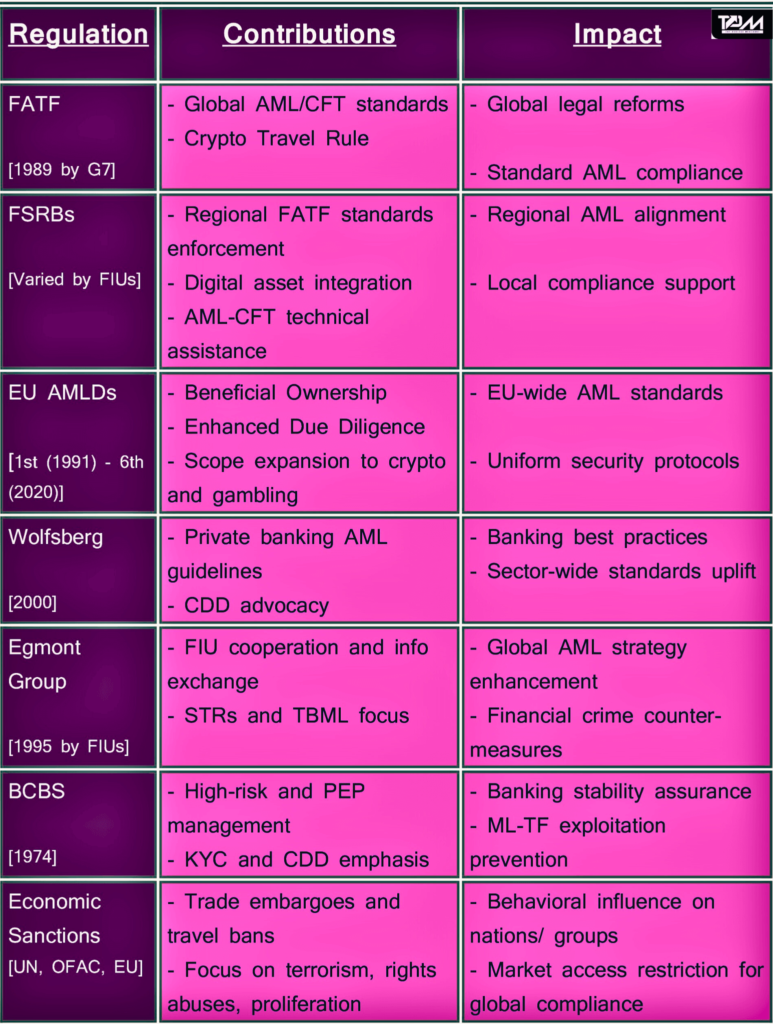

Financial Action Task Force (FATF)

The FATF stands at the forefront of the international effort to combat money laundering, providing a comprehensive set of AML compliance regulations. These regulations serve as a global benchmark, encouraging nations and financial institutions to implement rigorous AML banking regulations and practices.

Established: 1989 by the G7 to combat money laundering and terrorism financing.

Jurisdiction: Operates in 39 implementing jurisdictions including the Gulf Cooperation Council and the European Commission.

Key Contributions: 40 + 9 FATF Recommendations: Revised four times, addressing security standards against money laundering and terrorist financing.

Member Obligations: Implement and enforce stringent transaction monitoring protocols through Financial Intelligence Units (FIUs). Regulated institutions must monitor transactions and report suspicious activity through SARs and STRs to comply with AML/CFT regulations.

Crypto Travel Rule: Aims to regulate the movement of virtual currencies by requiring Virtual Asset Service Providers (VASP) to collect and share transactional information. This includes identity documents, customer ID, full name, address, and physical address. The 16th Anti-Money Laundering/Combating the Financing of Terrorism (AML/CFT) Recommendation also makes it mandatory for institutions to register users’ accounts with complete identity verification data.

How does the FATF influence global financial security?

By setting international standards and encouraging legal and regulatory reforms, FATF drives a coordinated global effort to prevent and combat money laundering and terrorist financing. The FATF seeks to produce the necessary ‘political will’ to bring about varied legal or operational measures across countries. Even though it is not binding, member nations must generally comply with the rules set forth by the FATF for an effective approach against money laundering on a global scale.

FATF Style Regional Bodies (FSRBs)

The FATF Style Regional Bodies (FSRBs) play a crucial role in translating global anti money laundering regulations into actionable regional policies. They ensure that the FATF’s standards are effectively adapted and enforced, enhancing regional AML regulatory requirements.

Established: The FATF Style Regional Bodies (FSRBs) were established to support the dissemination of the FATF Recommendations globally, with the first bodies forming after the FATF’s inception in 1989. The exact dates of establishment for each FSRB may vary.

Key Contributions:

Assist FATF by promoting the implementation of its 40+9 Recommendations regionally.

Conduct assessments on the implementation of FATF Recommendations.

Offer technical assistance and disseminate best practices for AML/CFT.

Help integrate digital assets like cryptocurrencies into financial systems.

Members: Includes regional organizations:

1. Asia/Pacific Group on Money Laundering (APG)

2. Caribbean Financial Action Task Force (CFATF)

3. Council of Europe Committee of Experts on the Evaluation of Anti-Money Laundering Measures and the Financing of Terrorism (MONEYVAL)

4. Financial Action Task Force of Latin America (GAFILAT)

5. Intergovernmental Action Group against Money-Laundering in West Africa (GIABA)

6. The Middle East and North Africa Financial Action Task Force (MENAFATF)

7. Eurasian Group (EAG)

8. Eastern and Southern African Anti-Money Laundering Group (ESAAMLG)

9. Task Force on Money Laundering in Central Africa (GABAC)

What role do FSRBs play in enhancing regional AML efforts?

FSRBs bridge the gap between global standards and local implementation, providing region-specific insights and support to ensure comprehensive compliance with FATF Recommendations. They are responsible for examining typologies and region-specific money laundering and terrorist activities, in addition to assisting FATF with guideline amendments based on their inputs.

European Union (EU) Anti-Money Laundering Directives (AMLDs)

The European Union’s Anti-Money Laundering Directives (AMLDs) exemplify the region’s commitment to advancing AML banking regulations. Each directive raises the bar for compliance, aligning the EU’s financial systems with the highest international anti money laundering regulations.

Establishment and Evolution: Progressed from the 1st AMLD (1991) focusing on basic money laundering crimes to the 6th AMLD (2020) addressing complex crime typologies, including protecting whistleblowers from bribery, corruption, and related malpractices.

Key Contributions:

Enhanced due diligence: Mandates thorough checks against terrorist financing and suspicious transactions.

Extends regulations to gambling sectors and crypto exchanges, emphasizing beneficial ownership data.

To establish stringent AML controls and protect the EU financial system from laundering activities.

How do AMLDs target evolving threats within the EU?

By updating and expanding the scope of regulations, AMLDs aim to counteract the increasingly sophisticated methods of money laundering and terrorist financing, ensuring a high level of security across the EU. The implementation of these directives in member states, expected to comply with set deadlines, helps to effectively control region-specific threats by setting up advanced prevention measures.

The Wolfsberg Principles

The Wolfsberg Principles set a benchmark for private banking, advocating for best practices in anti money laundering standards. These principles complement the FATF Recommendations, underscoring the banking sector’s commitment to AML compliance regulations.

Established: In 2000 by leading private banking institutions to set global AML guidelines for private banking.

Voluntary Adoption: While not mandatory, these principles are highly recommended for banking institutions worldwide. Prominent private banking institutions, including Bank of America, J.P. Morgan Chase, and HSBC, formed the initiative’s foundation.

Key Contributions:

Customer due diligence (CDD) guidelines to mitigate money laundering and terrorist financing.

The group frequently hosts policy briefings with international financial bodies such as The New York Clearing House, the European Banking Federation, and the International Banking Federation – all working towards mitigating criminal activity within the sector.

Why are the Wolfsberg Principles significant?

The Wolfsberg Principles are widely respected within the domain and are often cited alongside established commandments such as FATF, Basel Committee, and Transparency International CDD standards. They represent a collective effort by major banks to establish a uniform standard for AML compliance, promoting best practices in risk management and customer due diligence.

The Egmont Group of Financial Intelligence Units (FIUs)

The Egmont Group of Financial Intelligence Units (FIUs) is structured to enhance the global AML framework by facilitating cooperation and information exchange among Financial Intelligence Units (FIUs), critical for the effective implementation of AML regulatory requirements.

Established: In 1995 to facilitate international cooperation and intelligence sharing among national FIUs to combat money laundering and terrorist financing. The Egmont Group

Structure: Comprised of HoFIUs, Egmont Committee, Regional Groups, and Working Groups, including the Legal Working Group (LWG), Training and Communication, Outreach, Operational Working Group (OpWG), and IT Working Group (ITWG), each with specific duties.

Key Contributions:

Focuses on AML/CFT measures through suspicious transaction reports (STRs) and indicators for trade-based money laundering (TBML).

Indicators related to STRs involve large cash transactions, undefined political/influential fund transfers, or shell company activities.

Provides a platform for the exchange of expertise and financial intelligence among member countries.

How does the Egmont Group contribute to global AML strategies?

By facilitating international cooperation and information exchange, the Egmont Group enhances the effectiveness of national efforts to combat money laundering and terrorist financing.

Basel Committee on Banking Supervision (BCBS)

The Basel Committee on Banking Supervision (BCBS) contributes to the global financial stability by advocating for AML compliance regulations that ensure thorough customer due diligence and risk management in banking, reinforcing AML banking regulations at an international level.

Established: In 1974, to address global financial stability and quality banking supervision. Created by the G10 central banks and situated in Basel, Switzerland, at the Bank for International Settlements (BIS), though these operate as two distinct entities, BCBS gained increased attention in the late 90s with the globalization of the financial system.

Key Contributions:

Emphasizes KYC and CDD standards for banking relationships, including managing politically exposed persons (PEPs), numbered accounts, high-risk customers, and pooled accounts through their KYC policies.

These policies focus on aspects such as customer identification & screening against sanctions at the account opening stage, risk assessment on customers and transactions conducted through their accounts, record keeping and timely audits on customers’ activities, etc., thus enabling detection and prevention of money laundering.

Provides guidelines for managing high-risk customers, politically exposed persons (PEPs), and transaction monitoring.

What impact does the BCBS have on international banking practices?

BCBS guides worldwide financial stability and international financial market reform. Although voluntary, BCBS standards are widely adopted, promoting sound banking practices worldwide. By setting global standards for banking supervision, the BCBS plays a crucial role in preventing the banking sector from being exploited for money laundering and terrorist financing.

Economic Sanctions

Economic sanctions are vital tools within the international anti money laundering regulations, aimed at preventing financial crimes by targeting nations, entities, or individuals involved in illicit activities.

Established: Implemented by entities like the UN, OFAC, and the EU for political reasons, including trade embargoes and travel bans.

Key Contributions: Targets countries and organizations involved in activities such as terrorism, human rights abuses, and nuclear proliferation. Notable United States (UN) sanctions include those targeting:

Cuba for its dictatorship and Russia for its military aggression against Ukraine.

Sanctioned countries also include North Korea for sponsoring war and nuclear weapons proliferation,

Syria for endorsing terrorism, Afghanistan and others for illegal trade,

Iraq for terrorism financing, and Ethiopia, Libya, and South Africa for human rights abuses.

The UN has also issued economic sanctions against Somalia, due to political unrest.

How effective are economic sanctions in enforcing compliance?

Sanctions serve as a powerful tool for international diplomacy, influencing the behavior of nations and organizations by restricting their access to global markets and resources. Sanctions aim to coerce compliance with international norms and can be lifted once the sanctioned entity aligns with common goals and values. History has shown that these measures can effectively discourage certain activities or behaviors within an individual country or worldwide.

Key Global Anti Money Laundering Regulations In A Nutshell

Thus, the collective efforts of the above entities highlight the global commitment to strengthening AML compliance regulations. For businesses and financial institutions, steering these AML regulatory requirements is essential for maintaining integrity and trust in the global financial system.

Discover how Brazil’s COAF & BCB steer the nation’s compliance with crypto rules & AML-CFT requirements. – AML Regulations In Brazil

Final Word on Effective AML Compliance Regulations for Businesses

Achieving success in AML compliance often feels like maneuvering through a labyrinth of regulations, each challenging a step toward supporting people’s reliability on the economy.

Central to this endeavor are internationally recognized anti money laundering standards, including customer due diligence (CDD), know your customer (KYC), suspicious activity reports (SARs), and transaction monitoring. These practices are essential for keeping financial institutions aligned with global anti money laundering regulations.

As the financial sector evolves, so too must the strategies to protect it. A steadfast commitment to global anti money laundering regulations ensures that AML-CFT practices evolve in response to emerging threats and technological advancements. Over and above, AML compliance regulations are not static mandates, but dynamic foundations of our global financial system.

FAQs On Global Anti Money Laundering (AML) Compliance Regulations

What Is AML Compliance?

AML compliance regulations involves adhering to regulations designed to prevent and detect money laundering or terrorist financing activities. Financial institutions must develop and implement anti money laundering standards and compliance programs that include transaction monitoring, fraud detection, and payment screening, among other measures, to comply with the Bank Secrecy Act in the United States, the EU’s anti-money laundering directives, and other relevant legislation.

How To Check AML Compliance?

To check AML compliance, firms must ensure they have a comprehensive anti money laundering standards and compliance program in place as required by the Bank Secrecy Act and its implementing regulations. This includes conducting ongoing customer due diligence, monitoring for and reporting suspicious transactions, and keeping updated information on the beneficial owners of legal entity customers.

What Are the Current AML Regulations?

Current AML regulations vary by jurisdiction but generally include the Bank Secrecy Act in the U.S., the EU’s fourth and fifth anti-money laundering directives, and specific country laws. These regulations mandate financial institutions to establish AML programs, conduct due diligence, report suspicious activities, and comply with sanctions and watchlist screenings.

What Is Anti-Money Laundering Compliance Program?

Anti-money laundering or AML compliance regulations program refers to the adherence to laws that combat money laundering activities. This includes implementing internal controls and systems for detecting and reporting financial crimes, appointing an AML compliance officer, conducting independent audits, and providing ongoing employee training.

What Is the Purpose of the Anti-Money Laundering Act?

The purpose of the Anti-money laundering Act is to prevent and combat money laundering and terrorist financing by enhancing financial transparency, imposing obligations on financial institutions to detect and report suspicious activities, and ultimately protecting the integrity of the financial system.

What Are Anti Money Laundering Standards?

Anti money laundering standards include implementing written policies, designating a compliance officer, training employees, reviewing programs periodically, and conducting risk assessments. These standards aim to identify and mitigate the risks associated with money laundering and terrorist financing within financial institutions.

What Are Anti-Money Laundering Laws?

Anti-money laundering laws are regulations that require financial institutions to take proactive steps to detect and prevent money laundering and terrorist financing. These laws include requirements for customer identification, transaction monitoring, reporting suspicious activities, and conducting due diligence.

What Are Anti-Money Laundering Guidelines?

Anti-money laundering guidelines advise financial institutions on implementing effective AML compliance programs. This includes establishing written policies, conducting risk assessments, training employees, appointing a compliance officer, and performing ongoing monitoring and independent reviews to detect and report suspicious activities.

👉 Follow The Perfect Merchantfor Regular Global Anti Money Laundering Regulations Updates

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…