Transaction monitoring investigation is a cornerstone of anti-money laundering (AML) compliance for financial institutions and other AML-regulated businesses.

This piece outlines the core transaction monitoring steps required for businesses to fulfill AML compliance and avert financial crimes.

Key takeaways on transaction monitoring investigations steps. The steps involve:

continuously analyzing transactions,

identifying suspicious behavior, and

red flagging possible conduct of misdeeds

to capture money laundering, fraud, or other illicit activities.

A clear transaction monitoring process flow given below brings forth a clear picture of how these investigations are conducted. Now let’s start reading.

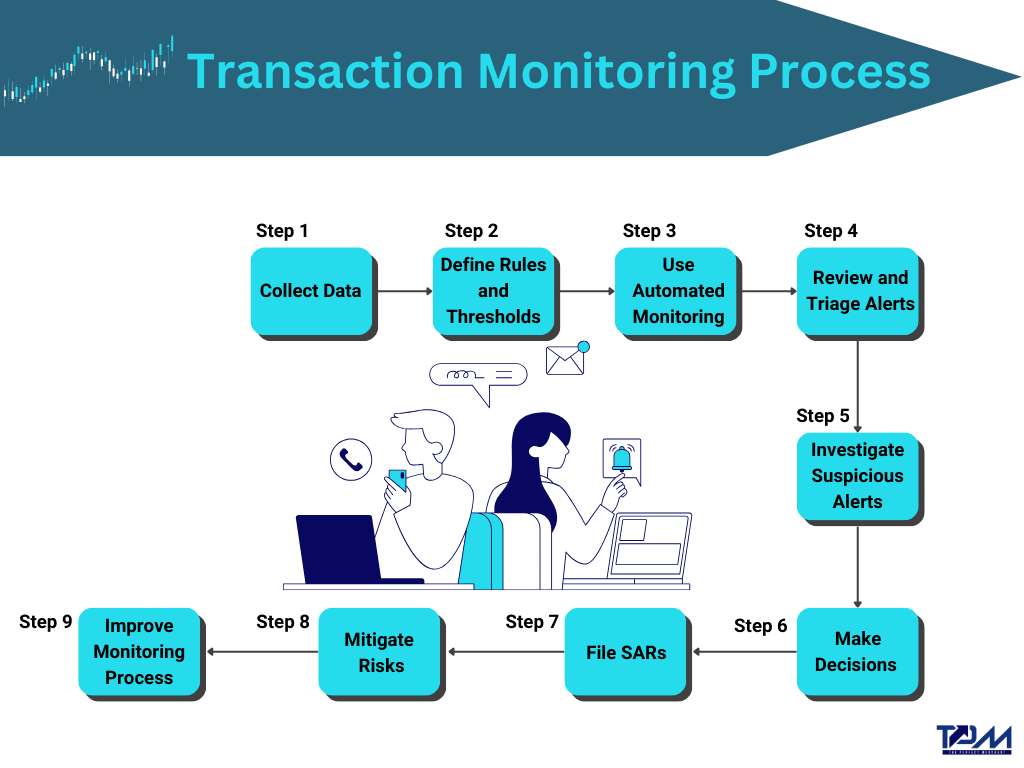

9 Transaction Monitoring Steps to Effective AML Investigations

1. Collect Comprehensive Customer and Transaction Data

A plausible transaction monitoring investigation begins with the collection of comprehensive data.

You need to gather detailed customer information, such as:

individual/business identity,

their account history,

business activities,

detailed transaction amounts,

transaction dates, and counterparties involved.

Against which data is the above information being compared?

Well, a transaction monitoring investigation system integrates data from both internal systems and external sources, such as sanctions lists and public records. This provides a holistic view of customer behavior and augments any investigator’s ability to detect suspicious activities competently.

2. Define Clear Rules and Thresholds for Monitoring

To effectively monitor transactions, you must establish clear rules and thresholds that define what constitutes suspicious activity.

The goal is to determine whether the transaction is genuinely suspicious and poses a risk or it’s a false negative.

6. Make Informed Decisions Based on Investigation Findings

After completing a detailed investigation, you need to decide whether the transaction is suspicious enough to warrant further action. This decision should be based on the evidence gathered during the investigation. If the findings indicate potential money laundering or other illegal activities, the investigation must proceed with appropriate measures, such as suspicious activity reporting (SAR) or account restrictions.

7. File Suspicious Activity Reports (SAR) to Authorities

When a transaction is confirmed to be suspicious, you must file a SAR with the relevant regulatory authorities or financial intelligence units (FIUs). This report should provide comprehensive details about the suspicious transaction, the parties involved, and the reasons for the suspicion. Timely and accurate SAR filings are critical to complying with AML regulations and contributing to broader efforts to combat financial crime.

8. Take Post-Investigation Actions to Mitigate Risks

After filing a SAR, consider additional actions to mitigate ongoing risks. These may include

strengthening monitoring of the customer’s activities,

implementing stricter controls,

or even terminating the customer relationship if warranted.

Post-investigation actions play a key role in preventing further suspicious activities and thus protecting the institution from potential exposure.

9. Continuously Improve the Transaction Monitoring Process

Finally, of course, AML threats are constantly evolving, and so should your transaction monitoring process.

Regularly review and update your monitoring rules and thresholds to reflect the latest regulatory guidance and emerging money laundering techniques.

Conduct periodic audits to assess the efficacy of your transaction monitoring steps.

Provide ongoing training to compliance staff to keep them informed of new threats and transaction monitoring best practices.

Final Notes on Transaction Monitoring Steps to Successful AML Investigations

One cannot deny that technology plays a significant role in effective transaction monitoring investigations.

Automated systems are indispensable for:

✔️ handling large volumes of transactions,

✔️ generation of timely alerts, and

✔️ screening transactions against established rules and thresholds.

However, it’s important to acknowledge that both technological tools and human judgment are required for the transaction monitoring process flow to work effectively.

✔️ While technology excels at identifying suspicious activities,

✔️ the expertise and discernment of compliance professionals are essential to

interpret these alerts,

conduct in-depth investigations,

and make sound decisions.

Thus, by combining technological advancements + human insight = effective defense against financial crimes for financial institutions.

We hope you enjoyed this article on transaction monitoring investigation steps. Stay tuned for more insights from ThePerfectMerchant!

Top FAQs on Transaction Monitoring Investigation

How can transactions be monitored? Transactions can be monitored using automated systems that flag suspicious activities based on predefined rules, patterns, and thresholds. These systems continuously analyze transaction data to detect anomalies.

What is the cycle of transaction monitoring? The transaction monitoring cycle includes data collection, alert generation, initial review, detailed investigation, decision-making, and reporting, followed by continuous improvement.

What are the six steps required to process a transaction? The six steps are authorization, authentication, transaction recording, validation, settlement, and reconciliation.

What is TM analysis in AML? TM (transaction monitoring) analysis in AML involves examining flagged transactions to identify patterns that may indicate money laundering or other illicit activities.

What are the transaction monitoring rules? Transaction monitoring rules are criteria set based on customer profiles, transaction types, amounts, and known risk factors to identify suspicious activities.

What to check in transaction monitoring? In transaction monitoring, check for unusual transaction sizes, frequency, geographical locations, counterparties, and deviations from normal customer behavior.

What is the process flow of a transaction? The process flow of a transaction typically includes initiation, processing, authorization, completion, and recording in financial statements.

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…