What Is AML Transaction Monitoring? (A Complete Guide)

How does AML transaction monitoring work? How does it fit into the bigger picture of financial safety, and why does taking a risk-based approach matter?

AML transaction monitoring is the financial sector’s powerhouse tactic against the scourge of money laundering and related crimes. When we peel back the layers on what is AML transaction monitoring, it’s essentially a vigilant system that tracks customer transactions—think deposits, transfers, withdrawals—to catch any odd or unusual activity that might hint at foul play.

Transaction monitoring in AML goes beyond mere compliance—it’s a cornerstone of ethical business practice. With governments tightening the noose on anti-money laundering regulations, any financial outfit skimping on a robust monitoring system is skating on thin ice. Imagine the chaos when sketchy transactions go unnoticed, spiraling into customer losses and a tarnished reputation that could spell the end for a business.

However, the essence of AML transaction monitoring is identifying red flags and creating a strong sense of trust and security around financial transactions. By analyzing transaction patterns and identifying any unusual activity, these systems help detect any suspicious activities and prevent criminal exploitation. These monitoring systems are essential in compiling reports for suspicious activities and play a decisive role in protecting the integrity of financial transactions against criminal activities.

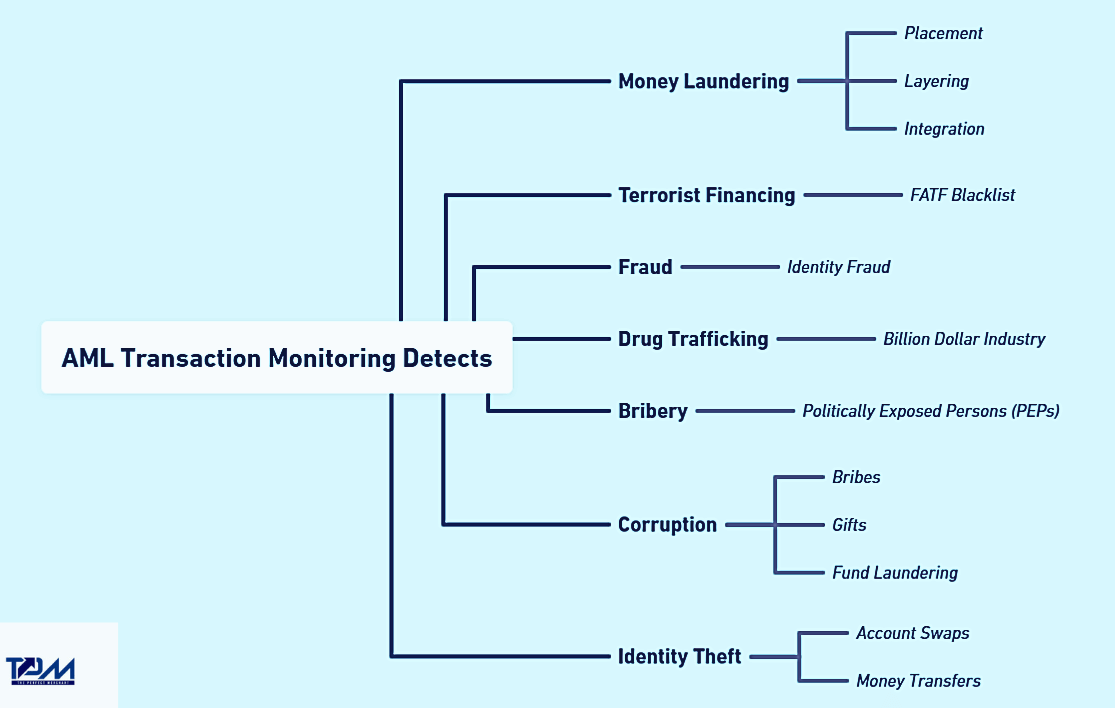

What Does AML Transaction Monitoring Detect?

AML (Anti-Money Laundering) transaction monitoring is a critical component for businesses, especially financial institutions, to detect and prevent illegal activities like money laundering and terrorist financing. Here’s a clear breakdown to help illustrate how it works:

Understanding the AML transaction monitoring process can help businesses maintain compliance and safeguard their operations.

How Does AML Transaction Monitoring Work?

AML transaction monitoring is an integral part of a financial institution’s compliance program, designed to identify and prevent illegal financial activities.

The process involves:

A detailed risk assessment.

Setting up tailored monitoring rules.

Regular optimization to improve detection accuracy.

Effective transaction monitoring relies on a combination of technology, human supervision, and ongoing refinement to adapt to changing risk environments. Let’s discuss this in detail.

1. Risk Assessment: Kickstarting the AML Compliance Program

The foundation of an effective AML transaction monitoring process begins with a thorough risk assessment. Financial institutions evaluate the potential risks associated with new and existing customers, as well as the products and services they offer. This step is about understanding the level of risk your institution is exposed to and ensuring you have the measures in place to manage it effectively.

2. Determining Suspicious Behaviors: Setting the Ground Rules

After assessing risks, the next move is to define what constitutes suspicious behavior within the context of your transactions. This involves setting clear parameters around unusual transaction patterns, such as large, sudden transfers, frequent transactions below reporting thresholds (to avoid detection), or dealings with high-risk entities. Recognizing these red flags is crucial for setting up an efficient monitoring system.

3. Creating Transaction Monitoring Rules and Alerts

Financial institutions develop specific transaction monitoring rules based on the risk assessment and definition of suspicious activities. These rules are designed to flag activities that may indicate potential money laundering, such as structuring transactions to evade detection or sudden spikes in account activity. When these rules are triggered, alerts are generated for further review.

4. Optimizing Rules Over Time: Enhancing Precision

A static rule set isn’t enough. Over time, as more transactions are monitored, insights gained can help fine-tune the rules to increase their effectiveness. This means adjusting rules to reduce false positives and better target genuine suspicious activities, making the transaction monitoring process in AML more efficient.

5. Investigations and Case Management

Upon receiving an alert, compliance teams spring into action, reviewing the flagged transactions to determine if they indeed signal suspicious activity. This step might involve reaching out to customers for clarification or conducting an in-depth investigation to understand the transaction context.

6. Filing Suspicious Activity Reports (SARs)

If an investigation confirms suspicious activity, the next step is to file a SAR with the Financial Crimes Enforcement Network (FinCEN) or the relevant regulatory body. This reporting is a crucial part of the AML transaction monitoring procedures, ensuring that potential criminal activities are communicated to the authorities for further action.

7. Ongoing Maintenance and Continuous Improvement

The AML transaction monitoring system is not a ‘set and forget’ solution. It requires regular updates and maintenance to adapt to emerging risks and regulatory changes. Continuous training for staff, periodic policy reviews, and collaboration across departments are essential to maintain a robust AML framework.

Thus, by understanding and implementing a comprehensive AML transaction monitoring process, businesses can comply with regulatory requirements and protect themselves and their customers from financial crimes.

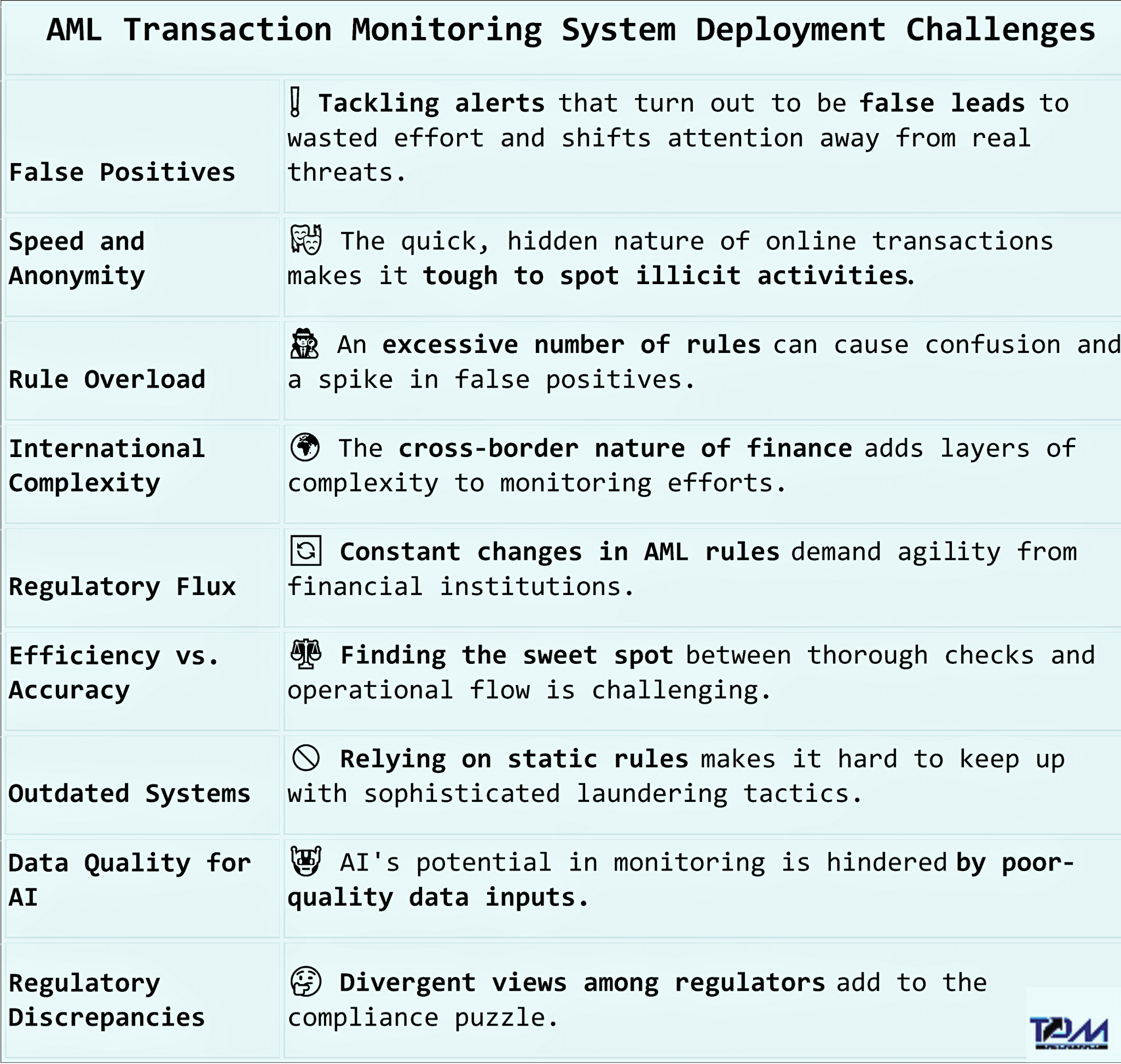

What Are the Main AML Transaction Monitoring Deployment Challenges?

AML Transaction Monitoring Systems are not merely about deploying cutting-edge technology but strategically integrating these technologies to create a responsive, adaptable, and comprehensive solution.

In the following section, we will discuss how an effective AML transaction monitoring system with advanced technology can be implemented to address the mentioned challenges with the help of suitable use cases.

Effective AML Transaction Monitoring Systems (And Their Case Studies)

AML transaction monitoring stands as a critical defense against financial crimes, confirming businesses stay compliant and vigilant. Understanding how AML transaction monitoring works involves recognizing the pivotal features that constitute an effective system. Let’s delve into the key components that make transaction monitoring systems effective and indispensable for businesses today.

· Flexible Rule Building

The essence of an efficient transaction monitoring process in AML is its adaptability. With financial crime tactics constantly evolving, the ability to quickly adjust and create dynamic, flexible rules is paramount. This agility helps minimize false positives—a common pitfall—while maintaining a keen edge on detection.

Case Study: For instance, a bank might adjust its transaction monitoring rules in response to a new type of fraud trend, such as the sudden rise in online payment scams during the holiday season.

· Integration of AI and Machine Learning

Incorporating Artificial Intelligence (AI) and Machine Learning into AML transaction monitoring solutions represents a significant leap forward. By analyzing complex patterns and behaviors beyond the reach of traditional rule-based systems, these technologies significantly reduce false negatives and unearth new, suspicious patterns, thereby broadening the system’s detection horizon.

Case Study: Consider a scenario where AI detects a pattern of small, frequent transactions late at night, which deviates from a customer’s usual behavior, signaling potential money laundering.

· Real-Time Monitoring and Alerts

An effective transaction monitoring system is characterized by its capacity for real-time monitoring and immediate alerts upon detecting suspicious activities. This feature is crucial for a prompt response, curtailing the opportunity window for illicit transactions to proceed undetected.

Case Study: Imagine a system that flags an unusually large wire transfer the moment it’s initiated, allowing for immediate review before the transaction is processed.

· Custom Rules and Flexibility

Customizable risk rules tailored to specific business needs and regulatory requirements highlight the system’s adaptability. This flexibility is essential for staying ahead in the ever-evolving financial crimes and regulatory environment.

Case Study: Given their high-risk nature and regulatory scrutiny, a fintech company might implement custom rules to monitor cryptocurrency transactions precisely.

· Data Capture and Logs

Robust data capture capabilities and comprehensive logs form the backbone of AML transaction monitoring systems, ensuring all activities are recorded. This is vital for regulatory reporting and supports data protection compliance.

Case Study: An investment firm could use detailed logs to trace the origin of a suspicious transaction during an audit, showcasing the transaction’s journey through various accounts.

· Velocity Rules

Velocity rules, which monitor the frequency and recurrence of user actions, provide deep insights into user behavior. They are especially useful for spotting suspicious activities that deviate from established patterns.

Case Study: Velocity rules might detect when a normally dormant account suddenly starts making frequent high-value transactions, indicating a possible account takeover.

· Holistic Customer Risk Assessment

A comprehensive approach to assessing customer risk, considering their entire profile and transaction behavior, allows for more accurate identification of potential risks and anomalies.

Case Study: A bank may notice that a long-standing customer with a previously impeccable record starts making transactions with high-risk jurisdictions, prompting a review.

· Reduction of False Positives

An effective monitoring system aims to reduce false positives, which can overwhelm compliance teams and distract from genuine threats, thereby enhancing the focus on high-risk transactions.

Case Study: A retail bank could refine its alert system to ignore regular large deposits from a known source, such as a customer’s monthly salary from a reputable company, reducing unnecessary investigations.

· Discovery of New Financial Crime Patterns

Utilizing AI and machine learning can uncover previously undetected patterns of suspicious behavior, giving businesses a critical edge in identifying and mitigating new threats.

Case Study: Machine learning could uncover a new scheme where fraudsters make transactions that mimic typical user behavior but with subtle anomalies, like slightly higher amounts or unusual timing.

· Integration and Breaking Down Data Silos

The ability to integrate with various data sources and platforms within an organization helps break down silos, providing a unified and comprehensive view of customer activities and risks.

Case Study: By integrating data across credit card, online banking, and loan departments, a bank might identify a fraud ring attempting to exploit vulnerabilities in multiple channels.

· Customer-Centric Approach

Analyzing the full spectrum of customer transactions and behaviors rather than isolated incidents enables a more accurate risk assessment and identification of illicit activities.

Case Study: A wealth management firm might analyze a client’s entire portfolio and transaction history to spot unusual trades that don’t align with their investment strategy.

· Data Mining and Anomaly Detection

Efficient analysis of vast datasets through data mining, combined with anomaly detection that leverages machine learning, significantly improves the system’s accuracy by pinpointing deviations from normal behaviors.

Case Study: Data mining could reveal an anomaly, such as a series of transactions just below the reporting threshold spread out over multiple accounts linked to the same individual.

· Leveraging Consortium Data Intelligence

Pooled anonymized data from various sources offers a broader perspective on customer behaviors, aiding in the detection of irregularities and unusual patterns, thereby strengthening the system’s ability to identify suspicious activities.

Case Study: Using shared intelligence from a banking consortium, a financial institution might identify a series of transactions linked to a newly identified fraudster operating across multiple banks.

Thus, by melding flexible rules, the analytical prowess of AI and machine learning, a holistic view of customer activities, efficient data mining, anomaly detection, and consortium data intelligence, businesses can forge a formidable defense against financial crime. This ensures compliance and protects the integrity of the financial system, securing the trust of customers and stakeholders alike.

Special Focus on Risk-Based Transaction Monitoring

Risk-based transaction monitoring stands out as a tailored strategy that resonates with the nuanced needs of diverse businesses. This approach, grounded in the principles set forth by the Financial Action Task Force (FATF), emphasizes a tailored monitoring process that aligns with the unique risk profiles of individual customers.

Here’s a breakdown of how the risk based transaction monitoring approach is reshaping transaction monitoring in AML:

I. Understanding the Risk-Based Approach

At its core, risk-based transaction monitoring is about applying a magnifying glass to your customers, evaluating them not as a monolith but as individuals with varying levels of risk. This methodology requires businesses to assess and respond to risks in a proportional manner, ensuring that high-risk customers undergo more rigorous scrutiny compared to their lower-risk counterparts.

II. FATF’s Guiding Principles on Risk-based Approach

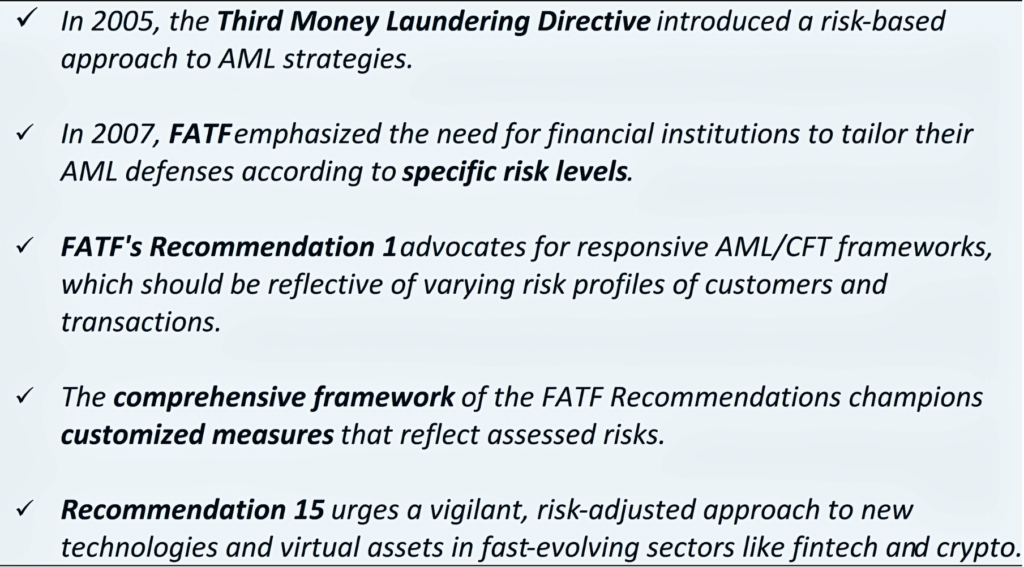

The Third Money Laundering Directive initially introduced the risk-based approach in 2005, which FATF later incorporated into its global recommendations. This approach has since become a cornerstone of AML regulations worldwide, emphasizing that AML controls should be proportionate to the perceived risk level of customers and the organization’s risk appetite.

The FATF introduced the risk-based approach in 2007, with its Guidance on the Risk-Based Approach to Combating Money Laundering and Terrorist Financing developed in consultation with the international banking and securities sectors. This approach has been central to the FATF’s recommendations for effectively combating money laundering and terrorist financing, emphasizing the need for financial institutions to assess and mitigate risks tailored to their operational context.

FATF’s Recommendation 1 lays the foundation by advocating for AML/CFT frameworks that adapt to customer and transaction risk levels. While Recommendation 1 directly emphasizes the need for a risk-based approach, the entire framework of the FATF Recommendations supports this principle by advocating for tailored measures based on the assessed risk levels of customers and transactions. This approach is fundamental to effective AML/CFT practices globally. Meanwhile, Recommendation 15 addresses the challenges posed by new technologies and virtual assets, urging a proactive stance in managing these emerging risks through a risk-based lens.

III. Key Elements of the Risk-Based Model

Implementing a risk-based transaction monitoring system involves several critical steps:

Customer Due Diligence: This initial step involves verifying identities and understanding the customer’s business, acting as the first line of defense in risk management.

Adverse Media Monitoring: Keeping an eye on external factors, such as a customer’s presence in negative media stories, can offer valuable insights into potential risks.

Sanctions Screening: Regularly screening customers against sanctions and watchlists ensures that businesses avoid entanglements with high-risk or sanctioned entities.

IV. Enhancing Due Diligence

The risk-based approach mandates differentiated due diligence efforts:

Simplified Measures for Low-Risk Scenarios: For customers or scenarios presenting minimal risk, streamlined due diligence can maintain efficiency without compromising security.

Enhanced Due Diligence for High-Risk Cases: In contrast, situations or clients deemed high-risk warrant intensified scrutiny, including more frequent reviews and deeper investigative efforts.

V. Implementing a Risk-Based Strategy

Adopting a risk-based transaction monitoring strategy involves two pivotal phases:

Risk Assessment: Identifying the level of risk associated with each customer sets the stage for all subsequent AML activities.

Tailored Due Diligence: Based on the assessed risk, businesses then tailor their due diligence processes, applying more stringent measures to higher-risk customers while simplifying procedures for lower-risk ones.

Thus, the risk-based approach to transaction monitoring in AML is not just a regulatory expectation. This nuanced approach allows businesses to allocate their resources more efficiently, focusing their efforts where the risk is greatest and improving the overall effectiveness of their AML transaction monitoring efforts.

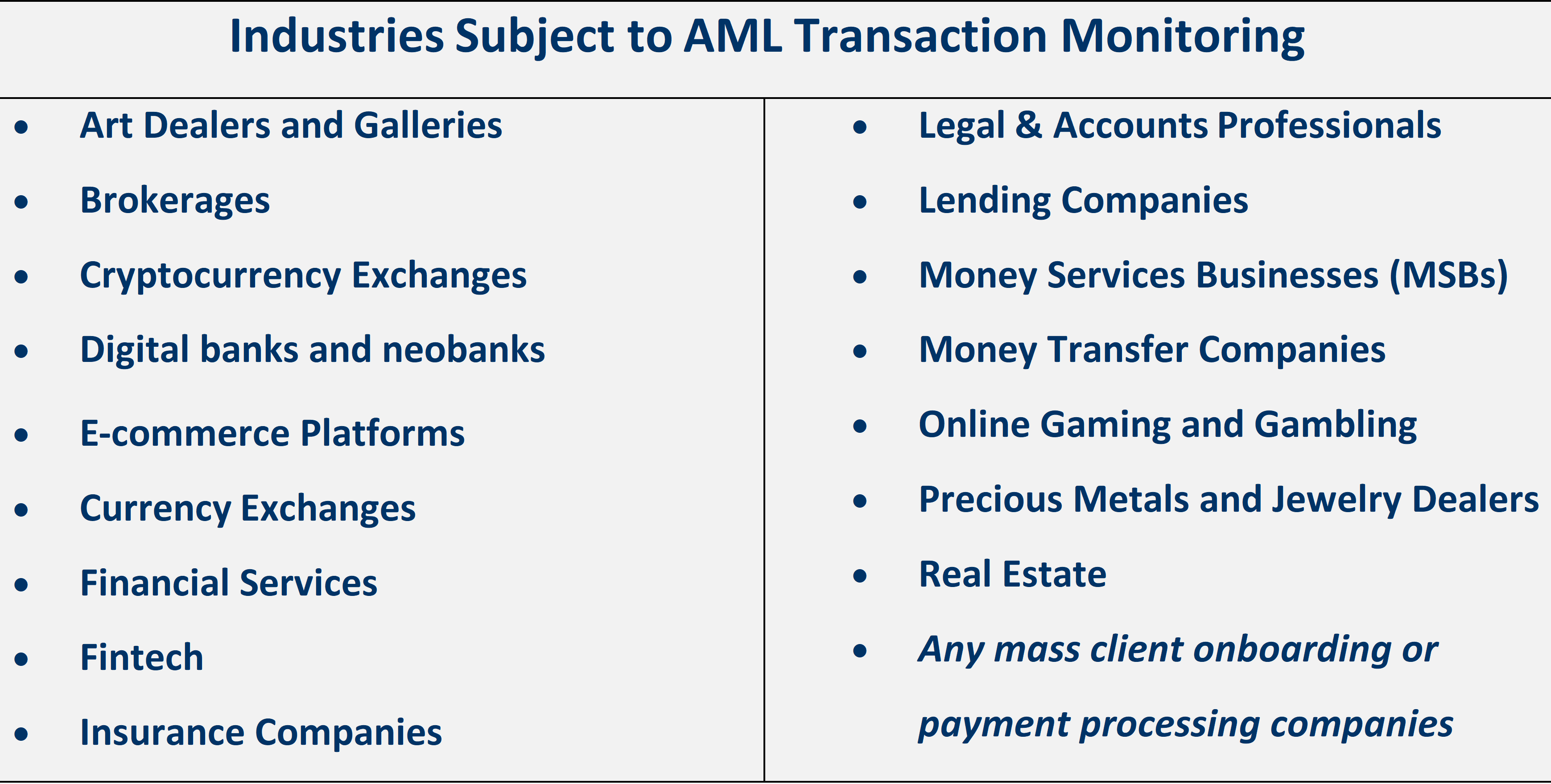

Which Industries Are Subject to AML Transaction Monitoring Compliance?

It’s essential for any company that moves money around to take steps to protect its customers from financial crime, fraud, and security breaches. This applies to various businesses, and each has a responsibility to implement effective measures to prevent financial crimes and protect their customers from harm.

How Does Transaction Monitoring Fit into AML Compliance?

AML transaction monitoring plays an integral role in a comprehensive compliance framework that checks and balances financial operations. To put it simply, it’s the part of the AML suite that scans for transaction anomalies, but it doesn’t work alone. It’s supported by a cast of processes that maintain the integrity of financial systems:

Transaction Screening: Acts as a gatekeeper, halting risky transactions at the door by cross-referencing sanction lists.

Client Screening: Regularly ensures clients are not listed in any adverse databases or involved in activities that could be cause for concern.

Client Activity Review: Keeps an ongoing check on clients’ transaction patterns for consistency.

Risk-Based Scorecard Review: Like a health check, it evaluates the risk level of transactions and client profiles, helping prioritize where to focus.

Together, these components form a comprehensive defense strategy. They’re not just a set of isolated tasks; they are interlinked steps in a company’s journey to remain compliant and secure. This approach enables businesses to confidently conduct operations while preventing financial crime.

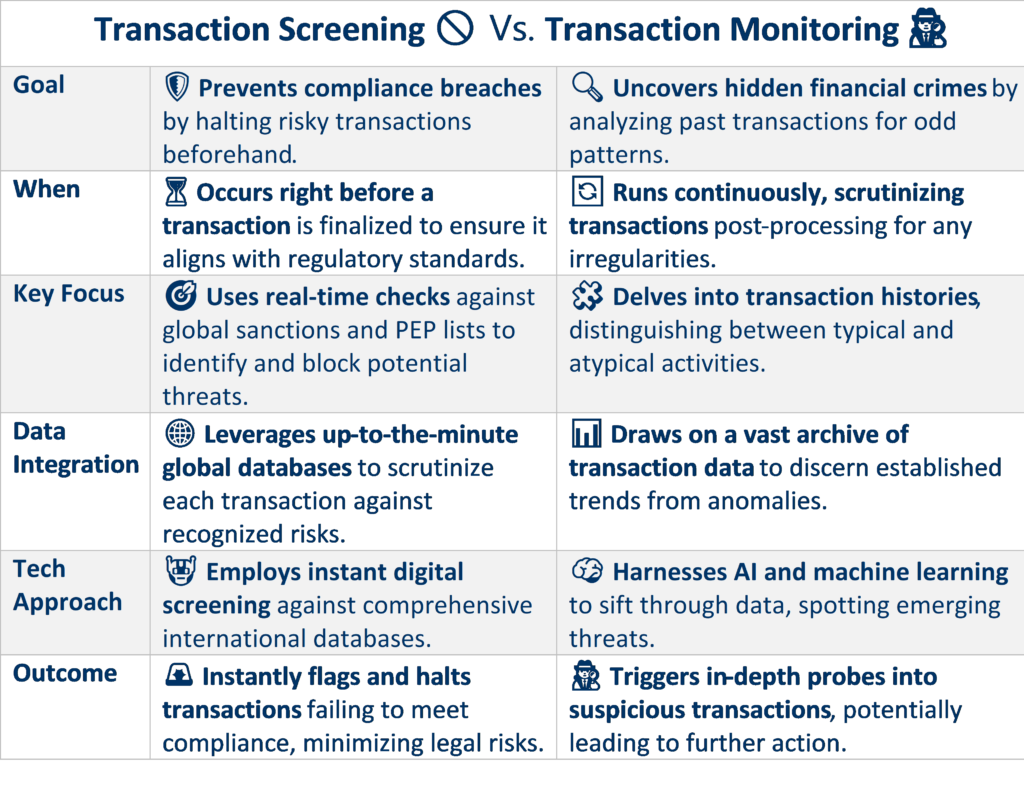

Transaction Screening Vs. Transaction Monitoring

Transaction Screening acts as a vigilant gatekeeper, weeding out non-compliant transactions before they proceed, while Transaction Monitoring casts a wider net, retrospectively sifting through transactions to flag those that need a closer look.

Both are pivotal to a robust AML/CFT framework, safeguarding against financial crimes and ensuring regulatory adherence with a harmonious rhythm that balances preemptive action with retrospective analysis.

Wrapping Up (With the Key Takeaways) on AML Transaction Monitoring Systems

As we round off our exploration of AML transaction monitoring systems, let’s reflect on the essentials. These systems are the financial sector’s seasoned detectives, constantly on the beat. They’re about keeping regulators at bay and are the cornerstone of a trustworthy financial marketplace.

Here’s the wrap-up:

Diligence is the watchword: Keeping a keen eye on each transaction ensures nothing slips through the cracks.

Adaptability is key: The financial world shifts daily, and so must our methods for safeguarding it.

Insight over oversight: The human judgment behind the tech often makes the difference between a red flag and a false alarm.

It’s a team effort: Every cog in the machine, from CDD to transaction analysis, works together to paint a complete picture of each client’s financial narrative.

On a final note, AML transaction monitoring isn’t a one-and-done deal. It’s an ongoing commitment to uprightness and transparency in a world where both are invaluable currencies. It’s about confirming that your business is thriving in a space where safety and integrity lead the way to success.

Top AML Transaction Monitoring FAQs

Why is AML monitoring important?

AML monitoring keeps financial systems clean by spotting shady money movements. It’s like a watchdog that barks at suspicious cash flows, helping keep things legit.

Why is AML transaction monitoring important?

It’s all about catching the bad guys by watching over transactions. Think of it as a detective that sniffs out fishy financial activities.

What is the difference between KYC and transaction monitoring?

KYC is like a first-time handshake, getting to know who you’re dealing with. Transaction monitoring is keeping an eye on their moves, making sure they play by the rules.

What is transaction risk in AML?

It’s the danger that comes with money moving in shady ways, potentially leading to financial crimes. It’s like walking on thin ice with your cash.

What is AML transaction monitoring in banking?

Banks use it to watch over money flows, catching any odd or risky transactions. It’s their way of keeping things clean and safe.

What are the benefits of AML transaction monitoring?

It helps banks stay on the right side of the law and builds trust with customers. Plus, it keeps their platforms from being playgrounds for money launderers.

What is transaction filtering in AML?

This is about blocking transactions that could break rules or sanctions. It’s like having a bouncer at the door, keeping the troublemakers out.

How do you conduct AML transaction monitoring?

You set up systems to spot and report weird transactions, using rules and patterns. It’s like setting a trap to catch financial mischief in the act.

If you’re keen to get the inside scoop on fighting money laundering and its precursor crimes, check out The Perfect Merchant. We are all about using smart tech to keep financial and non-financial businesses safe and sound.

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…