Stay updated on the AML risk-based approach. Read about the key elements of risk-based AML, its benefits, and the compliance framework. A must-read for all regulated entities.

Not all risks wear the same mask. An AML risk-based approach (RBA) means cutting through the noise to target the real money laundering (ML) and terrorist financing (TF) threats your organization faces.

An efficient AML risk-based approach helps organizations focus on resources that matter most: high-risk customers, products, and regions while streamlining efforts for lower-risk areas.

In this article, we will explore:

What is a risk-based approach in AML?

Key components of AML risk-based approach.

Major benefits of AML risk-based approach.

And risk-based AML from a regulatory perspective.

For AML-obligated businesses, juggling time and resources is a constant reality. This piece explains how a risk-based approach can help organizations comply with AML-CFT due diligence regulations at regional and international levels. Let’s get started!

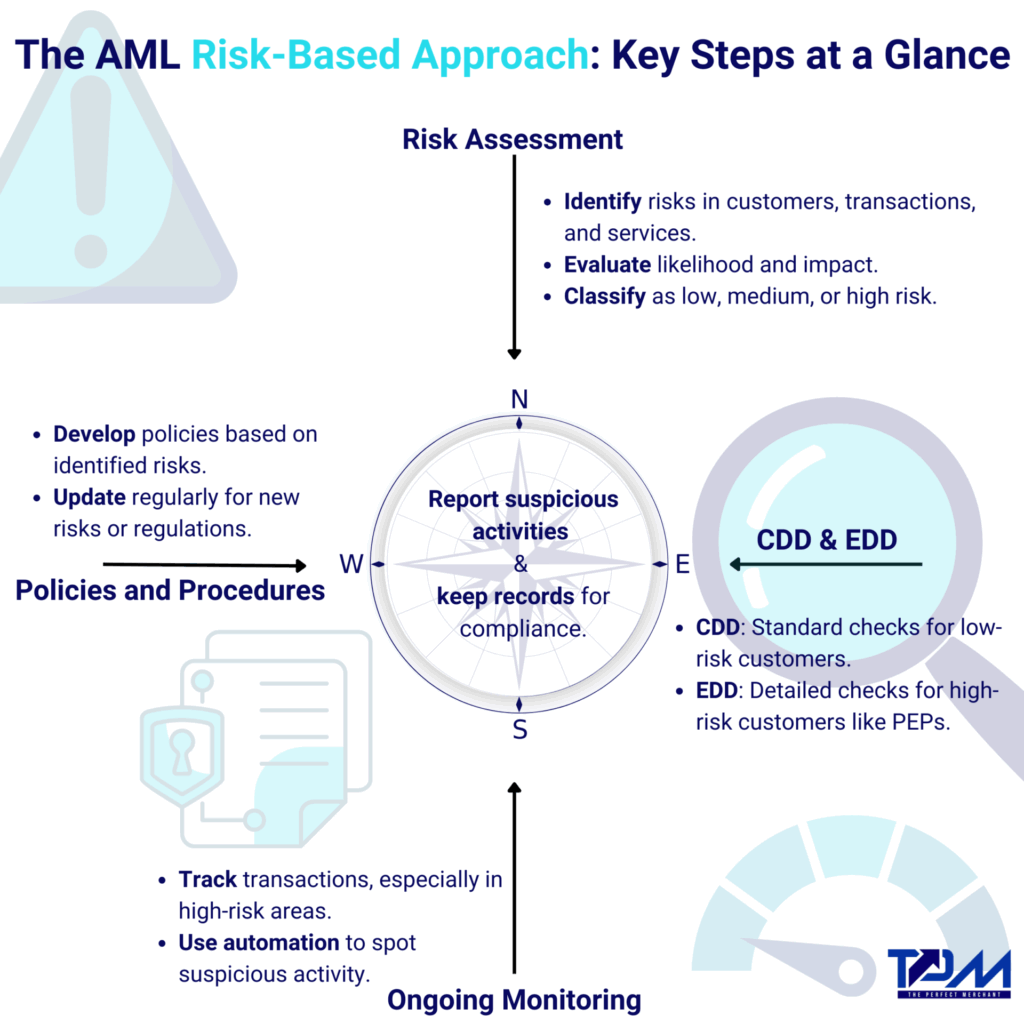

What Are the Main Elements of a Risk-Based Approach in AML?

There are five key parts to an AML risk-based approach, and we’ll break them down one by one to see how each helps manage money laundering risks.

1. Risk Assessment

Identify Risks: First, you need to figure out where money laundering or terrorist financing risks might be hiding. This could be based on who your customers are, the transactions they make, the products or services they use, or even where they’re located.

Identify Risks: Once you’ve found potential risks, look at how likely they are to happen and how big of a problem they could be. For example, consider high-profile customers, countries with weak laws, or services that move large sums of money.

Risk Rating: After that, group customers and transactions into categories like low, medium, or high risk. This helps you decide how much attention each one needs.

2. Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD)

CDD: For low-risk customers, you’ll do standard checks—like confirming who they are, understanding what they do, and watching their transactions.

EDD: For customers that pose a bigger risk (like politically exposed persons or those from high-risk areas), you’ll need to dig deeper. This might mean running more detailed background checks or tracking their transactions more closely.

3. Ongoing Monitoring

Keep an eye on transactions regularly to catch anything unusual. The more risky the customer, the more closely you’ll need to watch.

Automated systems can help you find patterns that might signal something suspicious.

4. Custom Policies and Procedures

Set up policies and controls that match the risks you’ve found. This might include watching transactions, training staff, and reporting anything suspicious.

Update your policies often to keep up with changing risks or new regulations.

5. Reporting and Record-Keeping

If you find anything suspicious, report it to the right authorities (like filing SARs).

Make sure you keep detailed records of your customers, the risks you’ve assessed, and the checks you’ve done, so you can prove you’re following the rules.

How AML Risk-Based Approach Benefits Obligated Entities

A risk-based approach gives AML-obligated businesses the flexibility to focus on what matters most—addressing the highest risks while keeping up with regulatory demands.

Smarter resource use: Instead of spreading your efforts thin, focus on the areas that carry the most risk. That way, you’re making the most of your resources.

Better compliance: By tailoring your AML efforts to the actual risks, you’ll be more likely to meet regulatory standards and avoid penalties.

Stay ready for change: A risk-based approach lets you adjust to new challenges—whether it’s evolving money laundering tactics or new threats that pop up.

Regulatory Perspective on AML Risk-Based Approach

Regulators, like the Financial Action Task Force (FATF) and national AML authorities, expect you to take a risk-based approach.

The FATF’s Recommendation 1 promotes this method, which means countries and financial institutions should assess the level of risk for money laundering and terrorism financing, and respond accordingly. Higher risks require stricter measures, while lower risks can have simpler controls.

With years of evolving research and analysis into money laundering and terrorism financing, regulators are well aware that not all customers, transactions, or products pose the same level of risk. That’s why they push for this method—to help you target and reduce risks more effectively and use your resources wisely where they are needed most.

Wrapping AML Risk-Based Approach

A risk-based approach to AML is about focusing your efforts where they’ll have the most impact. It means:

constantly reassessing risks,

adjusting your due diligence,

keeping a close eye on things, and

adapting as new threats come along,

—all to stay on top of money laundering and terrorist financing.

What is the first step in an AML compliance risk-based approach?

The first step is to figure out the money laundering and terrorism risks your organization faces. This means checking things like your customers, products, services, and locations.

What are the steps of the risk-based approach?

The steps are to find the risks, see how serious they are, put controls in place to handle them, and check if those controls work. This keeps happening to deal with new threats.

What is the BSA AML risk-based approach?

In the Bank Secrecy Act (BSA) approach, you first look for risks and rank them by how bad they are. Then, you use the right controls and resources to deal with those risks.

What is the AML risk model?

The AML risk model helps companies look at customers, transactions, and other factors to see how risky they are. Then, it puts them into low, medium, or high-risk groups for action.

What is the risk-based decision approach?

In this approach, decisions are made based on the level of risk. If the risk is higher, you use stricter controls. If it’s lower, you can use simpler processes to save time and resources.

What are the four types of risk in AML?

The four types of AML risk are customer risk, geographic risk, product/service risk, and transactional risk. These help you see where money laundering could happen.

What is the risk rating in AML?

Risk rating in AML means putting customers or products into low, medium, or high-risk groups. This helps decide how much you need to monitor them.

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…