Learn what is enhanced due diligence in AML? Discover how AML enhanced due diligence ensures compliance and identifies high-risk clients. Explore the roles of CDD and EDD in AML processes.

When it comes to anti-money laundering (AML), one significant aspect that businesses and financial institutions must grasp is enhanced due diligence (EDD).

Why is EDD so important?

Imagine you’re responsible for protecting your company against financial crime. Basic checks might work for everyday transactions, but what about high-risk situations? This is where EDD steps in.

In this piece, we’ll explore “What is enhanced due diligence in AML?”, examine its main features, and compare customer due diligence (CDD) with enhanced due diligence (EDD).

What is Enhanced Due Diligence in AML?

Enhanced due diligence (EDD) consists of AML procedures used by financial institutions and businesses to manage higher risks of money laundering and terrorist financing.

When a client or transaction poses a higher risk, EDD is applied to gather more comprehensive information, monitor activity more closely, and comply with legal requirements.

EDD isn’t simply a matter of fulfilling requirements; it’s about understanding the full picture of who you’re dealing with and the nature of their transactions. This helps prevent financial crimes and maintains the integrity of the financial system.

AML Enhanced Due Diligence Main Features

So, what makes EDD different from regular due diligence? Here are the key features:

1. Thorough Client Research for Background and Source Verification

This involves obtaining detailed information about –

the client’s background,

business activities, and

source of funds.

It often includes checking multiple sources and databases for verification.

2. Ongoing Transaction Scrutiny for Identifying Suspicious Behavior

EDD requires ongoing monitoring of the client’s transactions and activities. This helps –

monitor client’s business activities,

detect any unusual,

or suspicious behavior,

that might indicate money laundering or terrorist financing.

3. Advanced Identity Verification for Client Legitimacy

This means using advanced tools and techniques to verify the client’s identity and the legitimacy of their activities. This can include –

EDD (Enhanced Due Diligence): Used for higher-risk clients or transactions. It goes beyond standard checks to gather more comprehensive information, involves –

more rigorous monitoring,

and applies stricter verification methods.

It’s comparable to conducting a forensic audit when there are signs of financial irregularities, requiring more detailed scrutiny and validation to uncover any hidden issues.

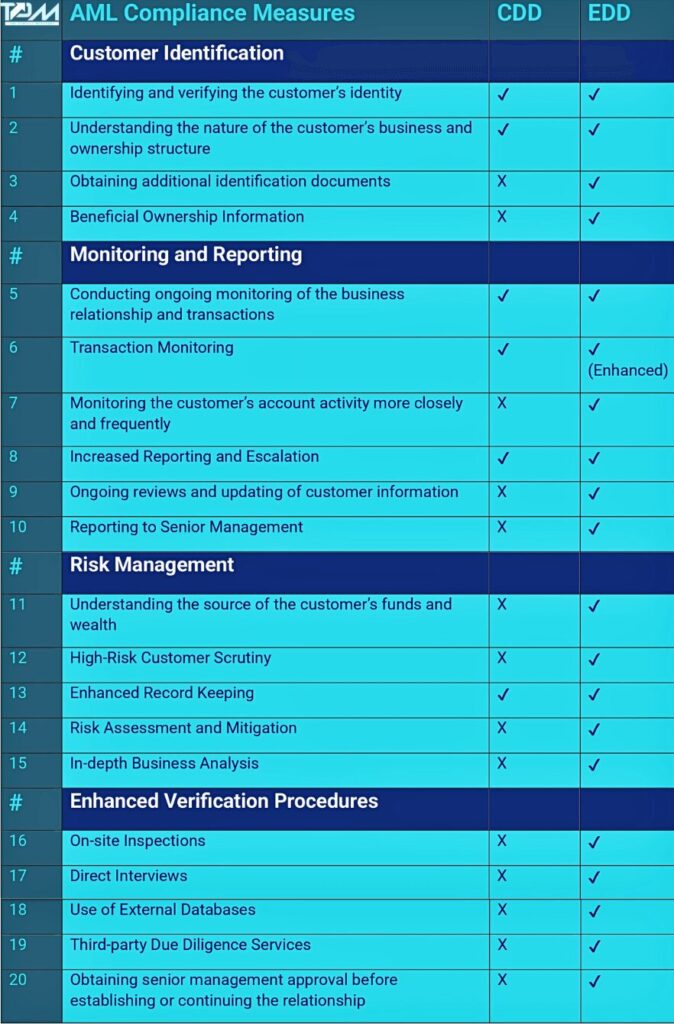

In essence, CDD is the foundation, and EDD builds on it when there are higher risks involved.

What additional steps are required in EDD that we don’t perform in CDD?

CDD and EDD in AML – A Comparative Overview

AML Enhanced Due Diligence Use Cases

AML enhanced Due Diligence (EDD) is applied in various high-risk scenarios to better manage and mitigate potential risks of money laundering and terrorist financing. Here are the key situations where EDD is essential:

Due diligence for politically exposed persons (PEPs): High-level scrutiny is required for PEPs due to their increased risk of involvement in corruption or bribery.

Monitoring clients from high-risk countries: Clients linked to countries with high levels of corruption or terrorism financing need additional due diligence.

Investigating complex ownership structures: When clients have opaque or unusually complicated ownership arrangements, EDD helps uncover the true beneficial owners.

Scrutiny of large or unusual transactions: Transactions that are significantly large or do not have an obvious economic purpose require deeper investigation to rule out money laundering.

Enhanced checks for cryptocurrency transactions: Due to the anonymous nature of digital currencies, enhanced checks are essential for transactions involving large sums or frequent movement of funds.

Final Thoughts on AML Enhanced Due Diligence

AML enhanced due diligence is an integral part of any effective AML compliance program. By understanding and applying EDD, businesses and financial institutions can better protect themselves against the risks of money laundering and terrorist financing. The focus is not only on meeting requirements but also on establishing a financial environment that is safer and more secure.

Ask yourself the following questions as you review your current AML procedures:

Do you have any high-risk clients or transactions that might require EDD?

What are the potential consequences of not conducting thorough checks?

✔️Fines?

✔️Reputational damage?

✔️Legal actions?

Next, consider the benefits of investing in EDD:

Protects your business against financial crimes

Builds trust with clients and stakeholders

Supports the long-term stability of your organization

Understanding and applying EDD could be the key to staying ready in the fight against financial crime and maintaining the long-term success of your business.

For additional insights on AML enhanced due diligence, fraud prevention, and cryptocurrency compliance, explore the comprehensive resources available on ThePerfectMerchant website. Follow us for regular updates and professional insights.

Top FAQs on What Is Enhanced Due Diligence In AML

What is the due diligence process in AML?

The due diligence process in AML includes verifying customer identity, understanding their financial activities, assessing risk levels, and ongoing monitoring to detect any suspicious transactions.

What are the three types of due diligence AML?

The three types of due diligence in AML are customer due diligence (CDD), enhanced due diligence (EDD), and simplified due diligence (SDD). CDD is standard, EDD is for high-risk customers, and SDD is for low-risk customers.

What is CIP vs CDD vs EDD?

CIP (customer identification program) verifies customer identity. CDD (customer due diligence) assesses risk and verifies identity. EDD (enhanced due diligence) is a deeper investigation for high-risk customers.

What is CDD and EDD in KYC?

In KYC, CDD (customer due diligence) involves basic identity verification and risk assessment, while EDD (enhanced due diligence) requires more detailed information and monitoring for high-risk customers.

What is the difference between AML CDD and EDD?

AML CDD is the standard procedure for verifying customers and assessing risk. AML EDD is a more thorough process for high-risk customers, involving deeper investigation and continuous monitoring.

Rachna Pandya

Rachna is a skilled Technical Content Writer specializing in financial crime prevention, with expertise in Anti-Money Laundering, Identity Verification, Sanctions Screening, Transaction Monitoring, and Fraud & Risk. She offers valuable insights and strategies through her content, particularly in Trade-Based Money Laundering, Transaction Monitoring, and Cyber Laundering.

“Once a PEP, always a PEP” is a rule that drives how banks and other financial institutions handle accounts for politically exposed persons (PEPs). The term PEP refers to people with public influence—like politicians or top government officials—who could misuse…

Spot AML red flags early, or risk letting trouble sneak through unnoticed. When every transaction counts, missing a sign isn’t just a slip—it’s a potential compliance risk. What Is a Red Flag in AML? A red flag in anti-money laundering…

Anti-money laundering compliance today means working with huge amounts of AML databases—from customer records and transactions to sanctions lists and watchlists. In this article, we’ll break down what an AML database is and its use cases to learn how AML…